AXISCADES: India’s Bet on Defence, Aerospace and AI Hardware

From aircraft design and mission computers to missile systems and AI infrastructure: why AXISCADES may be entering its most important growth cycle yet.

Before we begin, Check our Investorstack - Your one stop destination to become a better investor.

Here’s what you get:

Research Reports & Valuation models for more than 1000 companies!

Sector Intelligence Briefs

Industry Dashboards: Live RS ratings, dominant market stages, and sentiment across every industry.

Growth triggers, management consistency checks, walk the talk, thesis maps

and much more. Check out the landing page for an interactive demo.

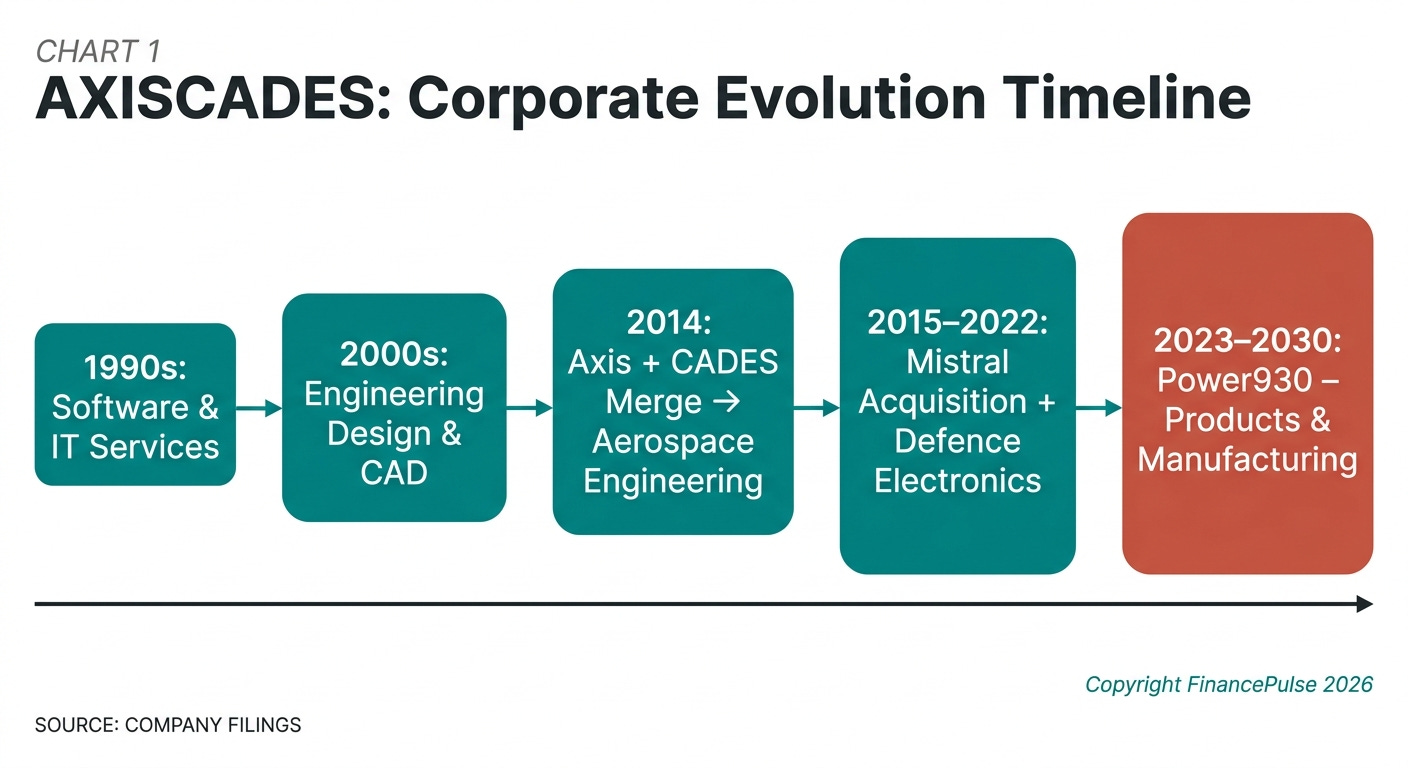

AXISCADES is a Bengaluru headquartered engineering and technology company that designs, develops, and increasingly manufactures products for aerospace, defence, and what it calls ESAI - Electronics, Semiconductors, and Artificial Intelligence. It was incorporated in 1990, originally as a software company catering to call centres and other early IT services. By the early 2000s, it had pivoted toward engineering design, setting up development centres and building a talent base in mechanical and electronics engineering. The name “AXISCADES” itself is a compound: Axis Mechanical Engineering Design (originally focused on automotive and heavy engineering CAD work) merged with Cades Digitech (which brought aerospace engineering capabilities) in 2014 to create the current entity.

When Airbus wants an external engineering team to help design aircraft structures, wire harnesses, or passenger-to-freighter conversion blueprints, AXISCADES engineers do that work from Bengaluru and Chester (UK). When the Indian Air Force needs avionics electronics for the Tejas Mk1A fighter jet, Mistral Solutions - AXISCADES’ wholly owned subsidiary - designs and manufactures the single-board computers and smart multifunction displays. When a hyperscaler building AI data centres needs thermal management systems for its servers, ADD Solutions (AXISCADES’ German subsidiary based in Wolfsburg) provides the engineering.

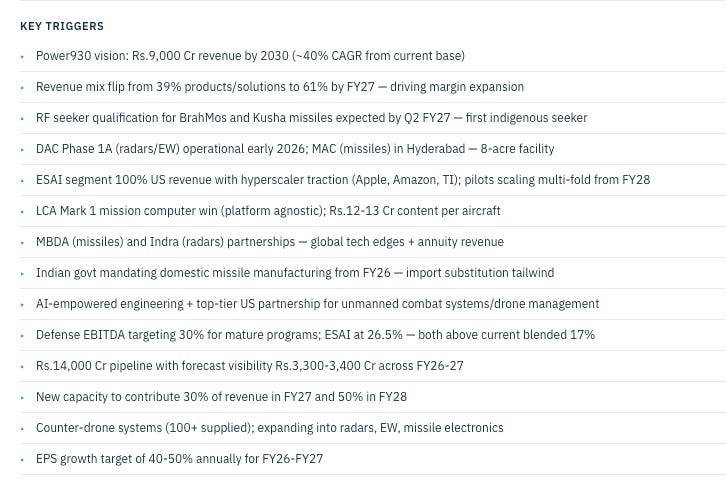

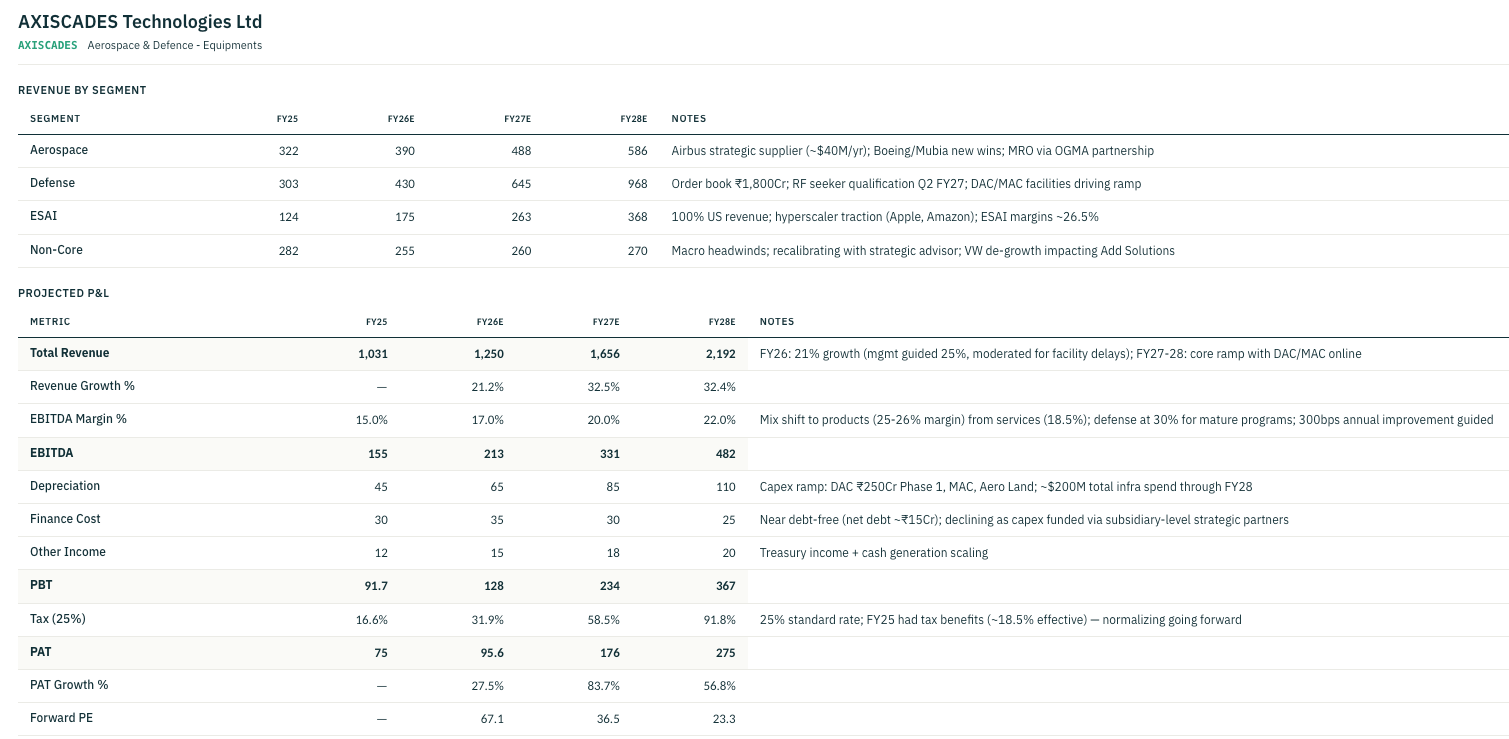

The company sits at a specific and strategically interesting point in the engineering value chain: it is not a pure-play services firm doing outsourced engineering hours (the old model), and it is not yet a full-scale manufacturer building finished platforms (such as HAL or BEL). It occupies the middle - product engineering, embedded systems design, and subsystem manufacturing - and it is actively pushing itself further into manufacturing and products. This transition is the central strategic bet of the current management, articulated as the “Power930” initiative: Rs. 9,000 crore in revenues by FY2030, from an FY26 run-rate of approximately Rs. 1,200-1,300 crore (extrapolated from 9MFY26 of Rs. 886 crore).

The founding logic of this transition is straightforward: services businesses are capped by headcount and have thin margins, while products and manufacturing create recurring, multi-decade revenue streams with significantly higher margins. A single-board computer sold to HAL for Tejas Mk1A might earn 25-40% EBITDA margins over a 15-30 year lifecycle. An engineering services contract delivering aerospace design work earns 12-15%. Management has explicitly targeted moving from roughly 50% services / 50% products today to over 80% products and solutions by FY28.

Business Segments

Aerospace

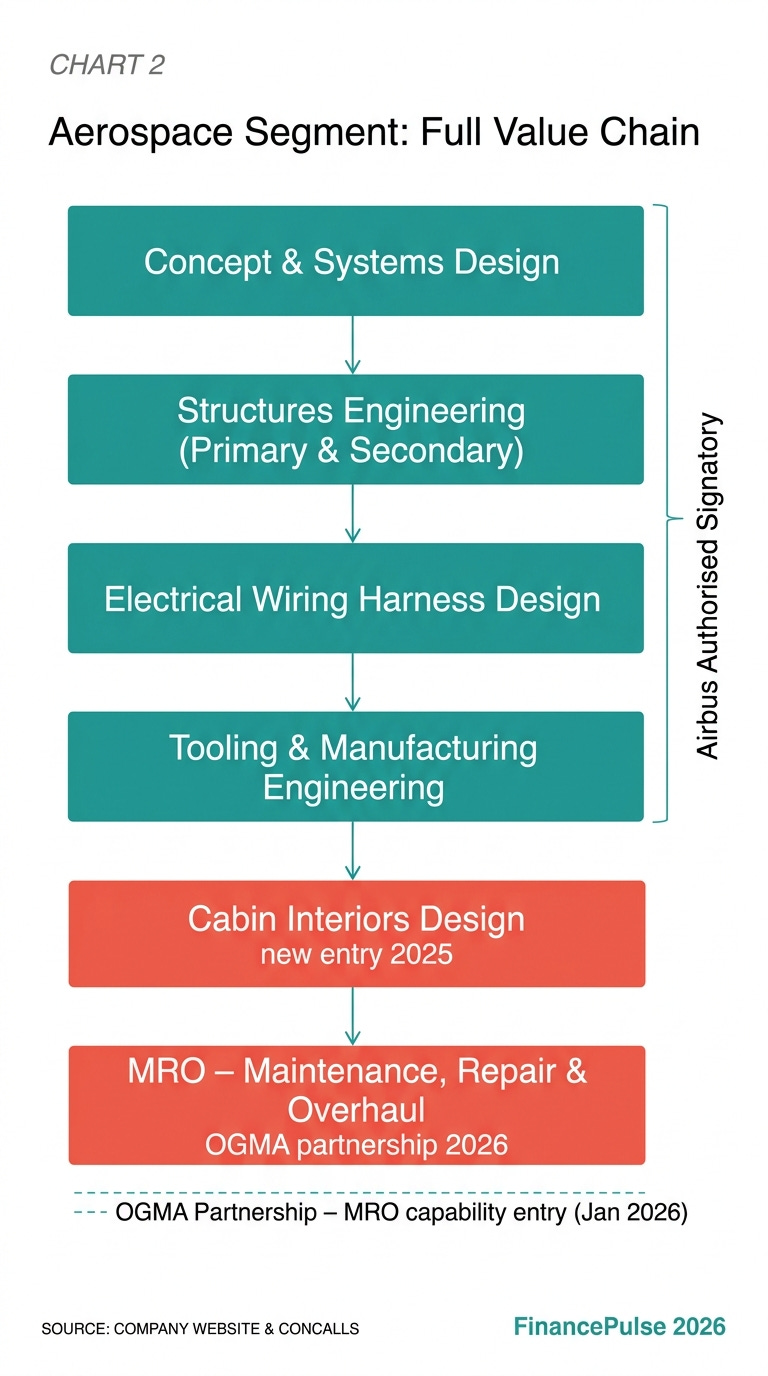

Aerospace is AXISCADES’ oldest core engineering services business, with a heritage stretching back to the Cades Digitech era. The company employs what it describes as the largest non-captive aerospace resource pool in India - engineers who work exclusively on aerospace programmes but for external clients rather than for a single captive OEM. This positioning matters: captive centres (like Airbus’ own Bengaluru engineering hub) can only serve one master, while AXISCADES can spread capacity across Airbus, Bombardier, and other OEMs simultaneously.

The primary customer relationship here is with Airbus. AXISCADES holds Airbus-authorised signatory status, meaning its engineers can sign off on certain design documents for Airbus aircraft - a certification that takes years to earn and creates real switching friction. The specific work includes electrical wiring harness design, primary and secondary aircraft structures, passenger-to-freighter conversion engineering, cabin interiors design (a new entry point added in September 2025 via pilot orders totalling USD 1.2 million from two global OEMs), and tooling design.

Bombardier is the second anchor relationship. AXISCADES has won the Bombardier Diamond Supplier Award for five consecutive years - an external validation of reliability and quality that the company uses actively in new customer conversations. Bombardier has been shrinking its global engineering footprint and has historically relied more heavily on third-party engineering partners like AXISCADES for work on its business jets.

The aerospace segment grew 28% year-on-year in Q3 FY26 and 12% in H1 FY26. The underlying driver is the commercial aerospace upcycle: Airbus is targeting 700+ aircraft per year in deliveries and has a backlog of over 8,000 aircraft to work through. For a company like AXISCADES, more aircraft production means more engineering work - structures design, wiring design, and tooling development - that gets pushed to cost-competitive offshore engineering partners.

A newer and potentially large avenue within aerospace is MRO (Maintenance, Repair, and Overhaul). India’s commercial aviation fleet is growing rapidly, and the country has historically sent most heavy maintenance work overseas because it lacked certified MRO facilities. In January 2026, AXISCADES signed an MoU with OGMA - Indústria Aeronáutica de Portugal (an Embraer subsidiary) - to jointly develop MRO capabilities in India. Through this partnership, AXISCADES gets access to OGMA’s global OEM certifications and its relationships with Airbus Defence, Rolls-Royce, and Pratt & Whitney. AXISCADES is building a large integrated aerospace and defence manufacturing and MRO hub near Bengaluru International Airport that will include dedicated aircraft hangars, engine shops, and a welding Centre of Excellence.

The company also has a design centre in Saltney, Chester (UK), which serves European aerospace customers and enables direct on-site engagement with Airbus and other British aerospace primes.

Defence (via Mistral Solutions and AXISCADES Aerospace & Technologies)

This is the highest-conviction segment for the company and arguably the most consequential bet. The defence story has two distinct layers: the longer-standing AXISCADES Aerospace & Technologies (ACAT) business and the more recently acquired Mistral Solutions.

ACAT focuses on defence engineering services - designing avionics, electronic warfare systems, radar and sonar systems, C4I2 (Command, Control, Communications, Computers, Intelligence, and Information) systems, and test solutions for the Indian Armed Forces and DRDO. This is design and development work, not manufacturing. ACAT has certifications under DO-254 (airborne hardware), DO-178 (software), and MIL-STD standards, and holds CEMILAC certification - these are the gating certifications required to participate in Indian defence programmes.

Mistral Solutions is the manufacturing arm, and the strategically more important entity. Acquired in a two-phase deal between 2017 and 2019 for approximately Rs. 200-300 crore, Mistral has over two decades of experience in defence electronics. Its product range includes signal and data processing units for radar systems, single-board computers (SBCs) for aircraft avionics, radar processing units for airborne early warning systems, telemetry modules, auto-pilot and mission computers, warhead control units, IGBT-based electronic control units, and FPGA/GPU-based computing engines.

The key insight about Mistral is the transition from prototype to production. In its earlier years, Mistral was primarily a prototyping house - designing defence electronics for DRDO programmes in early-stage development. This work is expensive and low-margin. As programmes mature and move into production, margins jump dramatically: management and independent analysis have cited 25-40% EBITDA margins on defence production orders versus single-digit or negative margins on early-stage prototype work. The company has explicitly guided that defence production revenues from Mistral were Rs. 112 crore in FY24, Rs. 170 crore in FY25, and targeted Rs. 225-250 crore in FY26.

The specific programmes AXISCADES is embedded in are the most significant in India’s indigenous defence build:

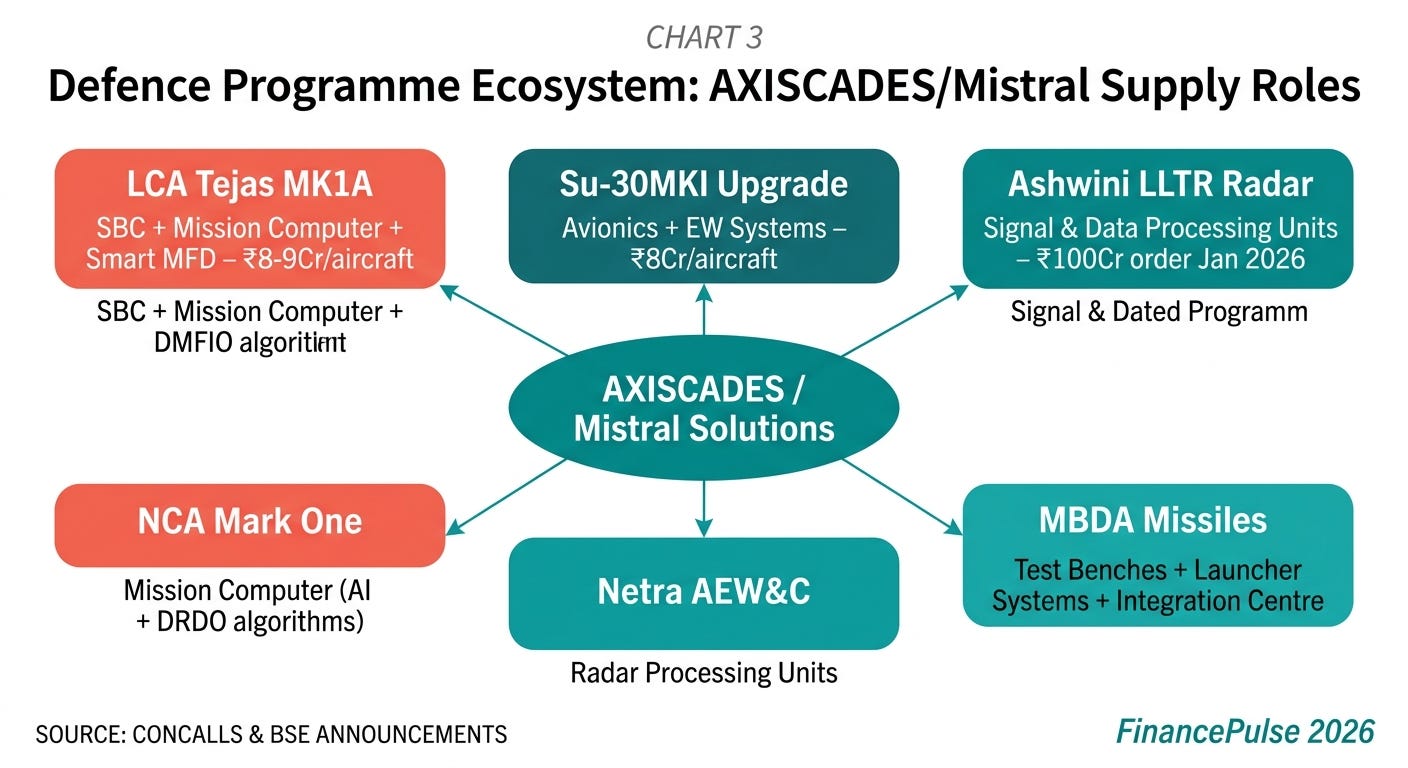

LCA Tejas Mk1A: The Indian Air Force has ordered 180 Tejas Mk1A aircraft for delivery by 2032. Mistral supplies single-board computers and avionics electronics for the Tejas programme and is expected to supply components for the Uttam AESA radar once it integrates from the 21st aircraft onwards. At roughly Rs. 8-9 crore of content per aircraft, the Tejas programme represents approximately Rs. 1,200-1,400 crore of potential revenue over the next 8-10 years. In February 2026, AXISCADES won an Rs. 80 crore order from HAL supplying the mission computer and smart multifunction display for LCA Mk1A.

Sukhoi Su-30MKI Upgrade: The Indian Air Force is conducting mid-life upgrades of over 100+ Su-30 jets. AXISCADES (through ACAT and Mistral) targets supplying upgraded avionics and electronic warfare components. This programme is estimated at a Rs. 2,000 crore opportunity and is expected to ramp from FY26 to FY28, with approximately Rs. 8 crore of AXISCADES content per aircraft.

LLTR Ashwini Radar: In January 2026, Mistral won a Rs. 100 crore contract from the LLTR Ashwini programme - India’s indigenous low-level transportable radar developed by DRDO and BEL - to supply signal and data processing units with liquid-cooling for extreme operational conditions.

MBDA Partnership: AXISCADES and MBDA have been collaborating for ten years, starting with test benches for the MICA missile. The relationship has expanded to include missile launcher systems, a new expanded test bench facility at Devanahalli, and plans for a dedicated MBDA system integration centre at the Devanahalli Atmanirbhar Cluster (DAC). At the Paris Air Show in June 2025, both CEOs publicly reaffirmed their commitment to expand under MBDA’s “Make in India” vision.

Netra AEW&C: India’s indigenous airborne early warning aircraft. Mistral supplies radar processing units; as India orders more Netra variants, Mistral stands to supply these components through Adani Defence (the prime contractor).

NCA Mark One Mission Computer: In Q3 FY26, management disclosed that AXISCADES is developing the mission computer for the NCA Mark One, described as platform-agnostic (usable across different aircraft platforms). The software combines algorithms from defence labs and AI algorithms developed by AXISCADES itself.

RF Seeker Development: Management disclosed in the Q3 FY26 concall (February 10, 2026) that AXISCADES is developing an RF seeker for larger missiles, including drones. Successful trials had been conducted, with full integration targeted by March 2026 and full qualification by Q2 FY27.

On the infrastructure side, the company inaugurated its 165,000 sq. ft. Devanahalli Aero Land (DAL) facility in Bengaluru Aerospace Park in FY26 - this is the manufacturing anchor for avionics orders including the LCA Mk1A production. The DAC (Devanahalli Atmanirbhar Cluster) adjacent to DAL will house radar integration hangars (expected Q3 FY27). Separately, AXISCADES acquired 8 acres in Hyderabad’s Aerospace Park for the Missile Atmanirbhar Complex (MAC) - to be set up in collaboration with an unnamed leading global missile manufacturer as technology partner, for large-scale production of next-generation missile systems.

Defence revenues grew 50% year-on-year in Q3 FY26 and 37% in Q2 FY26. Defence is now the primary growth driver for the company.

ESAI (Electronics, Semiconductors, and Artificial Intelligence)

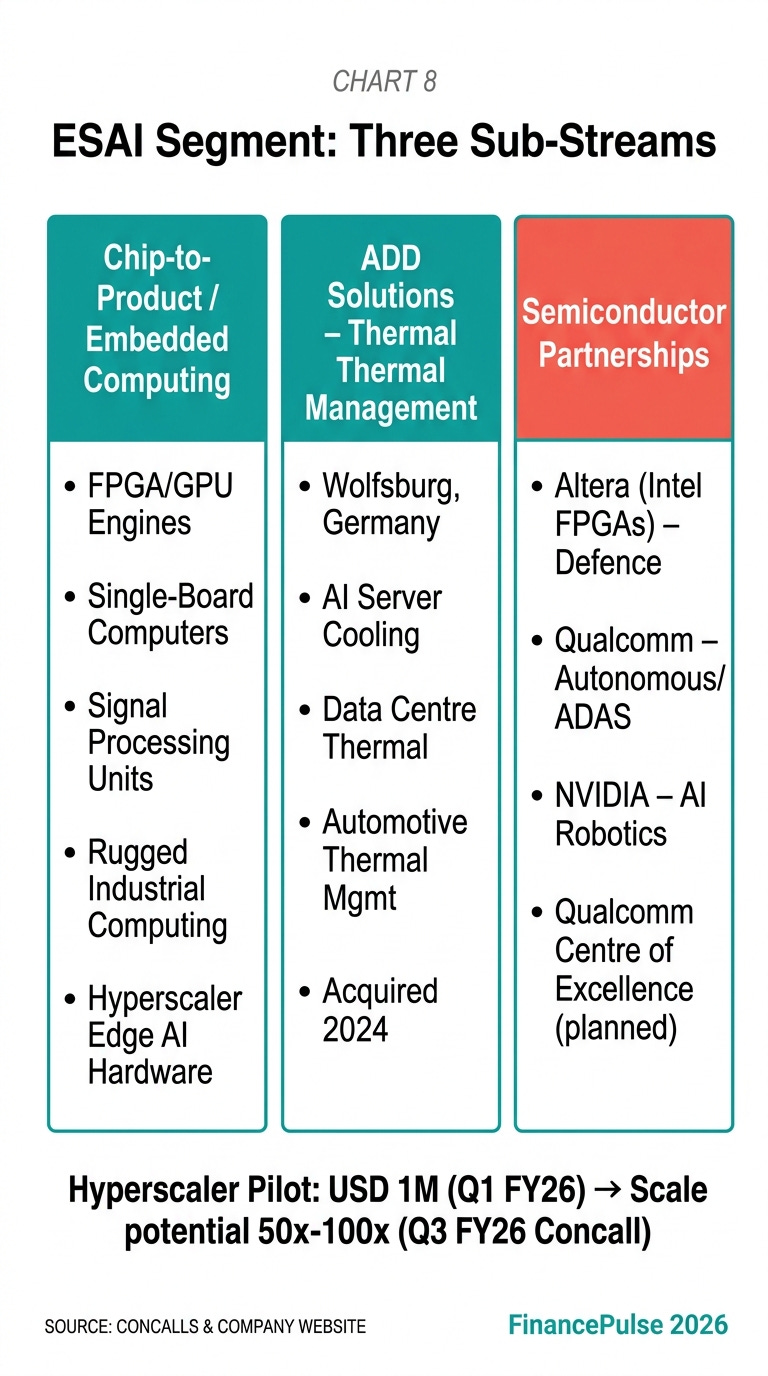

ESAI is the newest segment designation but represents a genuine expansion into adjacent markets that the company believes will scale faster than traditional engineering services. This segment sits inside Mistral Solutions and includes three distinct sub-areas:

Chip-to-Product / Embedded Computing: Mistral has deep expertise in building complete embedded computing systems - starting from chip-level design (FPGA-based, GPU engines, SBC architectures) through integration, box build, and deployment. The product catalogue includes signal processing engines, I/O boards, rugged graphics and single-board computers, FPGA and GPU engines, switches, storage systems, safety-critical middleware, and operating systems. This capability set makes Mistral a natural fit for hyperscaler customers who need customised, hardened computing for edge AI applications.

In Q1 FY26, AXISCADES’ ESAI team won pilot contracts with global hyperscalers worth approximately USD 1 million. Management described these in the Q3 FY26 concall as having potential to scale 50x to 100x once facility certification is complete and customers accept the volume production. The DAL facility’s advanced electronics manufacturing line is specifically being positioned for this opportunity. Multiple hyperscaler customer visits were planned for February and March 2026.

ADD Solutions (Wolfsburg, Germany): Acquired in 2024 from German firm ADD Solution GmbH, this entity specialises in thermal management systems for AI devices and data centres - specifically, solving the heat dissipation challenge that becomes critical as AI chip densities increase. As hyperscalers like Amazon, Google, and Microsoft invest hundreds of billions in AI data centre buildout, thermal management becomes an engineering bottleneck. ADD Solutions’ positioning at the intersection of automotive engineering (Wolfsburg is Volkswagen country) and AI infrastructure makes it unusual.

Partner Network for AI/Semiconductor: AXISCADES has formalised partnerships with Altera Corporation (Intel’s FPGA subsidiary) for FPGA-based defence applications, and with Qualcomm and NVIDIA for AI-enabled solutions in robotics, autonomous systems, and ADAS. These partnerships are still early but position AXISCADES in the reference design ecosystem for semiconductor platforms.

ESAI grew 18% year-on-year in Q3 FY26.

Legacy Segments (Heavy Engineering, Automotive, Energy)

These three segments represent the older AXISCADES core, and management has been explicitly pulling away from them in terms of strategic focus and resource allocation.

Heavy engineering is the oldest business - engineering design services for off-highway and industrial equipment manufacturers, with Caterpillar as a historically significant client. This is essentially a staffing-adjacent model - providing engineering headcount to OEMs who need flexible capacity. Margins have historically been thin (negative EBITDA at points) and the business requires scale to be profitable. Management has described this as a turnaround story moving from negative EBITDA to mid-single-digit EBITDA. Heavy engineering, automotive, and energy combined fell 8.5% year-on-year in Q3 FY26.

Automotive grew meaningfully in FY24 through the acquisition of ADD Solution GmbH (German market) and a long-term deal with a Tier-1 global automotive major. However, automotive software complexity (EV software, ADAS, cybersecurity) has created new opportunities alongside existing challenges from the global automotive capex pullback.

Energy is a small contributor - providing engineering services for oil and gas, renewables, and industrial energy clients. One notable win was an EPC major from the Middle East with a long-term contract signed in FY25.

Management has flagged that the “non-core” segments (heavy engineering, automotive, energy) are pulling down enterprise EBITDA margins, and the Power930 plan explicitly calls for these segments to either be fixed, restructured, or divested. As of Q3 FY26, management noted that non-core business divestment is “expected to be resolved by the next investor call.”

Products and Business Detail

AXISCADES operates a portfolio of products and services that are meaningfully different in their margin and growth profiles, which is core to understanding this business:

Engineering Services (Design, CAE, Manufacturing Engineering): This is the legacy model - engineers deployed to solve specific design problems for aerospace, heavy engineering, and automotive clients. Work includes mechanical design (using CATIA, Siemens NX, Creo), structural analysis (FEA, CFD), electrical wiring design, technical publications, and digital manufacturing engineering. These services are procured by global OEMs who need to scale engineering capacity without adding permanent headcount. Offshore delivery from India enables a 40-60% cost reduction versus equivalent European or North American engineering work. The company has authorised signatory status for Airbus engineering design work, which is the certification that allows AXISCADES engineers to finalise and sign off certain design packages rather than routing them back through Airbus engineers in Hamburg or Toulouse.

Embedded Systems and Defence Electronics: The Mistral product range. This is not commodity electronics - these are safety-critical, mil-spec hardware products designed to survive extreme vibration, shock, temperature, and electromagnetic environments. The design-to-qualification process for a defence electronics product takes 3-7 years; the manufacturing lifetime post-qualification can extend 15-30 years. This long-cycle nature creates sticky recurring revenues once in production. Notable product families include:

Signal and data processing units (deployed in radar systems like the Ashwini LLTR)

Single-board computers (deployed in avionics systems like LCA Tejas)

Mission computers (for fighter aircraft, now including the NCA programme)

Radar processing units (for AEW&C platforms like Netra)

Electronic warfare systems (countermeasures, jamming systems)

Smart multifunction displays (cockpit displays for fighter aircraft)

Test jigs and ATE (Automated Test Equipment) for defence programmes

Mission-Critical Infrastructure Products: AXISCADES has also moved into drones and counter-drone systems. Through its ACAT subsidiary, it offers custom drone solutions (heavy payload, armed, tethered), anti-drone systems, and mission-critical communication systems. It has signed partnerships with CILAS (France) for counter-drone directed energy solutions and Electronic Bird Control (EBC) for the e-Raptor biomimetic drone.

Manufacturing Facilities: The company is building a physical manufacturing infrastructure anchored around three nodes:

DAL (Devanahalli Aero Land): 165,000 sq. ft., fully operational, Bengaluru Aerospace Park - advanced electronics manufacturing, avionics production, hyperscaler edge computing prototype work

DAC (Devanahalli Atmanirbhar Cluster): Adjacent to DAL, radar integration hangars under construction (Q3 FY27 completion), MBDA system integration centre being set up

MAC (Missile Atmanirbhar Complex): 8 acres in Hyderabad Aerospace Park, in collaboration with an unnamed global missile manufacturer, for large-scale missile component manufacturing and integration

Geographic Presence: India (headquarters Bengaluru, offices in Hyderabad), France, Germany (Wolfsburg - ADD Solutions), Denmark, UK (Chester - Design Centre), USA (Fremont, California - Product Development Centre established 2025), and Canada. More than 3,000 professionals across 17 locations. The USA and Europe exposure gives it direct access to global OEMs for offshore engineering work while the India-based manufacturing infrastructure addresses the domestic defence indigenisation opportunity.

Customers

AXISCADES’ customer base splits cleanly into two categories by segment: global commercial OEMs (primarily Western aerospace majors) and the Indian defence establishment. These two sets have fundamentally different buying behaviours.

Airbus: The single most important commercial relationship. AXISCADES holds Airbus authorised signatory status for engineering design - this is a multi-year certification that requires demonstrating consistent quality, process discipline, and technical depth. Airbus is running at capacity trying to deliver aircraft against a multi-thousand-aircraft backlog; its response to this pressure is to push more design work to trusted offshore partners. The fact that Airbus has authorised AXISCADES to sign off certain engineering deliverables (rather than reviewing everything internally) is the most concrete evidence of the depth of this relationship. Airbus accounted for a significant portion of aerospace segment revenues.

Bombardier: The company has won Bombardier’s Diamond Supplier Award five consecutive years as of 2025. Bombardier is a business jet manufacturer that relies more heavily on third-party engineering partners (relative to commercial aircraft OEMs) because its programmes are smaller-scale. AXISCADES works on design, structures, and interiors engineering for Bombardier programmes.

HAL (Hindustan Aeronautics Limited): The primary domestic defence customer. HAL manufactures the Tejas Mk1A and Su-30MKI. Mistral’s LCA Mk1A orders flow through HAL - three separate production orders have been announced in recent months, two for single-board computers (Rs. 25 crore each) and one for the mission computer and smart multifunction display (Rs. 80 crore).

DRDO and BEL: The Ashwini LLTR radar order (Rs. 100 crore) flows through this channel - DRDO designs the radar, BEL is the prime manufacturer, and Mistral supplies signal and data processing units as a subcontractor.

MBDA: The European missile systems company. A 10-year relationship that started with test bench design for the MICA missile and has grown to include missile launcher systems and (in progress) a dedicated MBDA system integration centre at AXISCADES’ DAC facility.

Indra: Strategic alliance signed in 2025, with Indra establishing a Centre of Excellence at the DAL facility. Indra is a Spanish-headquartered European defence and aerospace major.

Hyperscalers (unnamed): Pilot contracts worth USD 1 million won in Q1 FY26, with management describing these as having 50x-100x scaling potential as the DAL facility gets certified. The customers have not been publicly named.

Caterpillar: Anchor heavy engineering customer, providing engineering services for off-highway and construction equipment design.

Customer concentration risk: The top two clients reportedly account for approximately 73% of standalone revenues. This is a material risk that management is explicitly trying to reduce through the diversification strategy - adding hyperscaler customers, new defence programme wins, and new European aerospace relationships.

Contract structure: Defence production contracts are typically multi-year supply agreements with defined quantities per year (for example, the Ashwini radar contract is a two-year execution). Engineering services for commercial OEMs tend to be ongoing frameworks with periodic purchase orders. The long-term nature of defence programmes (LCA Mk1A deliveries expected through 2032, Su-30 upgrade programme through 2028+) provides multi-year revenue visibility once a company is qualified on a platform.

Switching costs: For defence electronics, switching is extremely expensive. Once a single-board computer or mission computer is qualified on a specific aircraft platform and certified by CEMILAC, replacing it requires re-qualification of the entire system - a process that can take 2-4 years and is not initiated unless absolutely necessary.

Competitive Landscape

In defence electronics: The direct competitors for Mistral’s products include Data Patterns (India), Astra Microwave, Bharat Electronics (BEL), and some international suppliers. BEL is the dominant PSU player but is increasingly capacity-constrained and unable to serve all the demand from India’s indigenisation push. Data Patterns and Astra Microwave are the most comparable listed private-sector players. The key differentiators for Mistral are: (1) the depth of design capability, going all the way to chip-level FPGA design rather than just integration; (2) the specific programme wins already embedded in platform qualifications (once you are qualified on Tejas, the qualification itself is a barrier); and (3) the manufacturing infrastructure (DAL facility) now being built to scale production.

In aerospace engineering services: The relevant competitors are Tata Technologies, Cyient, and QuEST Global. Tata Technologies is the largest, with a strong automotive and aerospace engineering services book. Cyient has historically been strong in aerospace MRO engineering and electronics. QuEST Global (unlisted) is significant in aerospace engineering services globally. What AXISCADES has that these competitors do not is the Airbus authorised signatory credential and the direct tie-up with Bombardier. What AXISCADES lacks relative to Tata Technologies is scale, balance sheet strength, and the brand recognition of the Tata Group.

In the ESAI / Semiconductor / AI hardware space: This is a nascent competitive position. Companies like Persistent Systems, L&T Technology Services, and global FPGA/embedded design boutiques compete here. ADD Solutions’ thermal management positioning is more unique - there are few Indian companies with deep thermal management for AI hardware expertise.

Barriers to entry in defence: The most important barriers are not capital but credentials. CEMILAC certification (for defence airborne systems) takes years to acquire. Design wins on platform programmes (like Tejas or Ashwini) require established DRDO and services relationships that cannot be replicated quickly by a new entrant. The combination of engineering capability, manufacturing infrastructure, and programme relationships that AXISCADES has built through the Mistral acquisition and its own ACAT subsidiary represents a 20+ year accumulation that a new entrant would struggle to replicate in under a decade.

Barriers in commercial aerospace: Airbus authorised signatory status is a concrete, certification-based barrier. The five consecutive Bombardier Diamond Supplier Awards represent demonstrated execution reliability that matters when an OEM is deciding which offshore partners to extend work to. Building this track record takes a decade.

Where AXISCADES is more vulnerable: In pure engineering services (non-defence), the competition is intense and margins are under pressure from larger players with more scale. In the legacy heavy engineering and automotive segments, the company is unambiguously not a preferred partner and has been losing ground to lower-cost and better-scaled competitors.

Industry

India’s defence indigenisation: This is the most important tailwind for the next five years. India has formally committed to reducing its defence imports from roughly 70% of procurement to under 30% by 2025 and has a “positive indigenisation list” of over 300 items that must be procured domestically. This list includes complex electronics like radar subsystems, avionics, and mission computers. The combination of:

An active LCA Tejas Mk1A production programme (180 aircraft, delivery by 2032)

Su-30MKI mid-life upgrades (100+ aircraft)

New programmes in the pipeline (AMCA - Advanced Medium Combat Aircraft, AEW&C expansion, Tejas Mk2, Light Combat Helicopter production ramp)

A defence budget that crossed Rs. 6.2 lakh crore in FY24 and has been growing consistently

Creates a structural multi-decade demand pool for the specific products that AXISCADES/Mistral makes. The key constraint is not demand - it is supply-side: can Indian defence electronics firms qualify their products, scale their manufacturing, and deliver reliably?

Global commercial aerospace: Airbus and Boeing together have a combined backlog exceeding 15,000 aircraft as of early 2026. Production rates are recovering after COVID disruptions and are expected to ramp materially through 2030. Each increment in Airbus production rate requires more engineering work to be distributed to offshore partners. The recent problems at Boeing (737 MAX safety concerns, production slowdowns) have indirectly benefited Airbus by pulling more orders toward it.

The India aerospace and defence market was valued at USD 26.78 billion in 2023 and is expected to reach USD 48.41 billion by 2032, growing at approximately 6.8% annually. The specific electronics and embedded systems sub-segment (where Mistral competes) is growing faster than the market aggregate because it is the segment experiencing the strongest indigenisation-driven demand substitution.

Import dynamics: India currently imports most sophisticated defence electronics - radar signal processors, mission computers, avionics systems - from the US, France, Russia, and Israel. Government policy is explicitly trying to replace these imports with domestic production. The positive indigenisation list and defence acquisition procedures that favour domestic suppliers create a regulatory tailwind for companies like AXISCADES that can deliver these products domestically.

Growth Triggers

LCA Tejas Mk1A production ramp: Management disclosed in the Q3 FY26 concall that AXISCADES is embedded in the Tejas Mk1A avionics supply chain with supply content of approximately Rs. 8-9 crore per aircraft. The programme is expected to reach full rate production of 16-24 aircraft per year from FY27 onwards, with indigenous avionics (including the Uttam radar) integrating from the 21st aircraft. At full rate, this programme alone could contribute Rs. 150-200 crore annually to defence revenues.

Su-30MKI upgrade programme: In the Q2 FY26 concall, management noted “significant order book for execution in FY25 and FY26” and highlighted the Su-30 upgrade as a key driver of defence revenue growth. With content of approximately Rs. 8 crore per aircraft and 100+ jets to be upgraded, this represents a Rs. 800-1,000 crore cumulative opportunity ramping from FY26 through FY28.

DAL facility hyperscaler certifications: Dr. Sampath Ravinarayanan stated in the Q3 FY26 concall that the DAL facility has attracted two global leaders who have established exclusive laboratory and production spaces. Pilot hyperscaler orders of USD 1 million have potential to scale 50x-100x once facilities are certified, with multiple customer visits planned for Q4 FY26. If even a fraction of this scaling materialises, it represents a significant new revenue stream.

Missile complex buildout: AXISCADES has acquired 8 acres in Hyderabad’s Aerospace Park for the Missile Atmanirbhar Complex in collaboration with a leading global missile manufacturer. The MAC will be dedicated to missile component manufacturing, integration, seekers, onboard electronics, and data links. Production is expected to commence from FY28 and could represent the single largest product manufacturing scale-up in the company’s history.

OGMA MRO partnership: The January 2026 MoU with OGMA gives AXISCADES access to certification pathways for complex MRO work on Embraer, Airbus Defence, Rolls-Royce, and Pratt & Whitney platforms. This is a several-year development but opens a new revenue stream that does not currently exist.

ADD Solutions - Automotive and AI Thermal: Management noted in the Q1 FY26 concall that “ramp up in high-end cybersecurity solutioning with UK automotive manufacturer” was underway and that the ADD Solutions acquisition brings access to global OEMs in automotive and AI thermal management.

Key Risks

Customer concentration: The top two customers are reported to account for approximately 73% of standalone revenues. This creates substantial revenue and relationship risk. If either of these two relationships deteriorates - through quality issues, changes in OEM strategy (such as bringing work back in-house), or competitive displacement - revenue and margin impact would be severe and immediate.

Government defence procurement cycle: India’s Defence Acquisition Procedure (DAP) is complex and slow. Contracts are often delayed by 1-3 years from programme approval to first order. A company like AXISCADES invests in manufacturing capacity in anticipation of these orders; if orders are delayed or quantities are reduced, the capacity investments become loss-making overheads. The Ashwini radar order of Rs. 100 crore is a two-year execution contract - if the programme is extended or rephased, Mistral’s production capacity remains idle.

Non-core margin drag: The heavy engineering, automotive, and energy segments are actively pulling down enterprise-level margins. Management has been restructuring these for multiple quarters without a definitive resolution. If these segments cannot be fixed or divested, they will continue to dilute the attractiveness of the core defence and aerospace business.

Capex overrun and debt risk: The Power930 plan requires substantial capital investment across DAL, DAC, and MAC. Management indicated in the Q2 FY26 concall that funding will come from “internal accruals, strategic investments by our partners, and some bridge funding from the bank.” With a consolidated net worth of approximately Rs. 700 crore and net debt of Rs. 50 crore at Q2 FY26, the balance sheet can absorb some capex, but any sustained shortfall versus plan could require additional equity dilution or debt.

ESAI scaling uncertainty: The hyperscaler opportunity is genuinely large but dependent on DAL facility certification - which is new and untested. Hyperscalers typically require multiple certification rounds, quality audits, and pilot productions before committing to volume purchase orders. Management’s statement about 50x-100x scaling potential is aspirational and dependent on execution milestones that have not yet been achieved.

Scenarios & Valuation

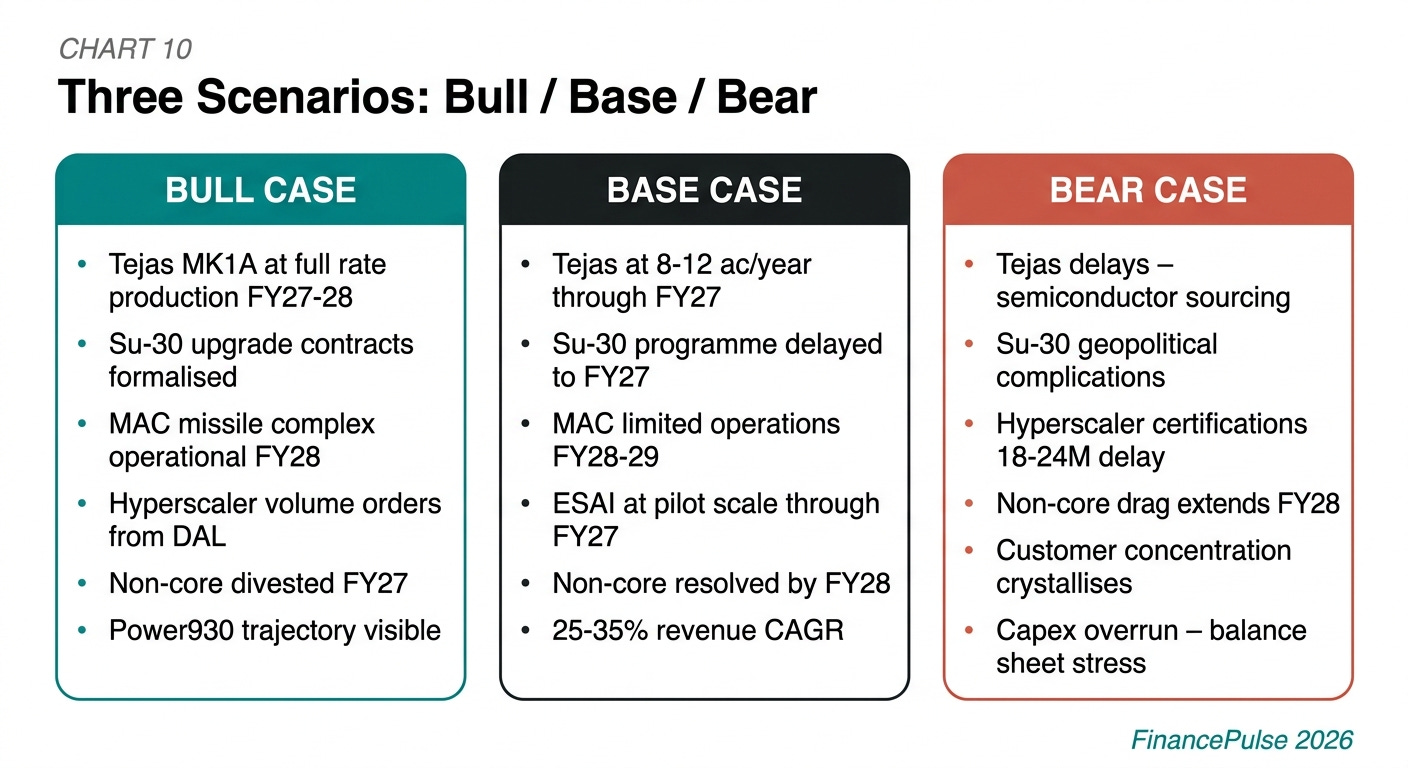

Bull Case

India’s defence indigenisation accelerates ahead of schedule. The Tejas Mk1A production ramp reaches 20+ aircraft per year by FY28, with the Uttam AESA radar integrating from Jet 21 onwards - delivering AXISCADES Rs. 150+ crore annually from this programme alone. The Su-30MKI mid-life upgrade programme contract is formalised and ramps to full execution. The Missile Atmanirbhar Complex in Hyderabad commences missile component production in FY28 as planned, in collaboration with the unnamed global missile manufacturer.

On the ESAI front, the DAL facility’s hyperscaler customers move from pilot to volume production, with one or two hyperscaler names making significant long-term commitments for edge computing hardware. ADD Solutions’ thermal management business wins two or three large data centre cooling engagements from US or European hyperscalers, creating a recurring product-revenue stream from a high-growth end market.

The non-core segments (heavy engineering, automotive, energy) are either divested or restructured to breakeven by Q1 FY27, removing the margin drag. Enterprise EBITDA margins move from the current 18% (core) to 22-24% as products and manufacturing become the majority of revenue. The Power930 trajectory to Rs. 9,000 crore becomes visible in the financial results rather than just management guidance.

Base Case

Defence indigenisation proceeds at its historical, somewhat slower pace. Tejas Mk1A deliveries remain at 8-12 aircraft per year for FY27, with full rate production pushed to FY28-FY29. Su-30MKI upgrade programme formalisation takes until FY27. The missile complex commences limited operations in FY28-FY29. Revenue from these three programmes grows materially but below the most optimistic scenarios.

ESAI hyperscaler work remains at pilot/prototype scale through FY27 as facility certifications take longer than management expects. The commercial aerospace services business continues growing at 15-20% per year, underpinned by the Airbus backlog execution and Bombardier programme work.

Non-core segments take until FY28 to fully resolve (either fixed or sold). Enterprise margins improve gradually, reaching 17-19% by FY27. Revenue grows at 25-35% annually through FY27, making the company clearly larger, but the Power930 Rs. 9,000 crore target requires sustained execution in FY28-FY30 from programmes that have not yet commenced at scale.

Bear Case

Programme delays pile up. The Tejas Mk1A programme faces further semiconductor sourcing challenges or HAL production bottlenecks, delaying revenue recognition and leaving the DAL facility operating below capacity. The Su-30MKI upgrade programme stalls due to geopolitical complications around Russian-platform work. The hyperscaler facility certifications take 18-24 months longer than planned.

The non-core segment drag continues because no viable divestiture buyer emerges at acceptable terms, and the restructuring drags into FY27-FY28. Customer concentration risk crystallises when one of the top two customers reduces its offshore engineering outsourcing.

The capex programme (DAC radar hangars, MAC missile complex) runs over budget or schedule. Management’s bridge financing requirement grows, and either dilutive equity is raised or debt rises meaningfully above the current Rs. 50 crore net debt. The Power930 target remains a long-term aspiration rather than a visible near-term trajectory.

Thanks for reading! Do check out Investorstack.