Azad Engineering: Riding the Turbine and Aerospace Cycle

How a turbine blade supplier built a global OEM moat and why capacity expansion could unlock the next phase of growth

Before we begin, Check our Investorstack - Your one stop destination to become a better investor.

Here’s what you get:

Research Reports for more than 1000 companies!

Sector Intelligence Briefs

Detailed Valuation Models for companies

Industry Dashboards: Live RS ratings, dominant market stages, and sentiment across every industry.

Growth triggers, management consistency checks, walk the talk, thesis maps

and much more. Check out the landing page for an interactive demo.

Now onto today’s piece.

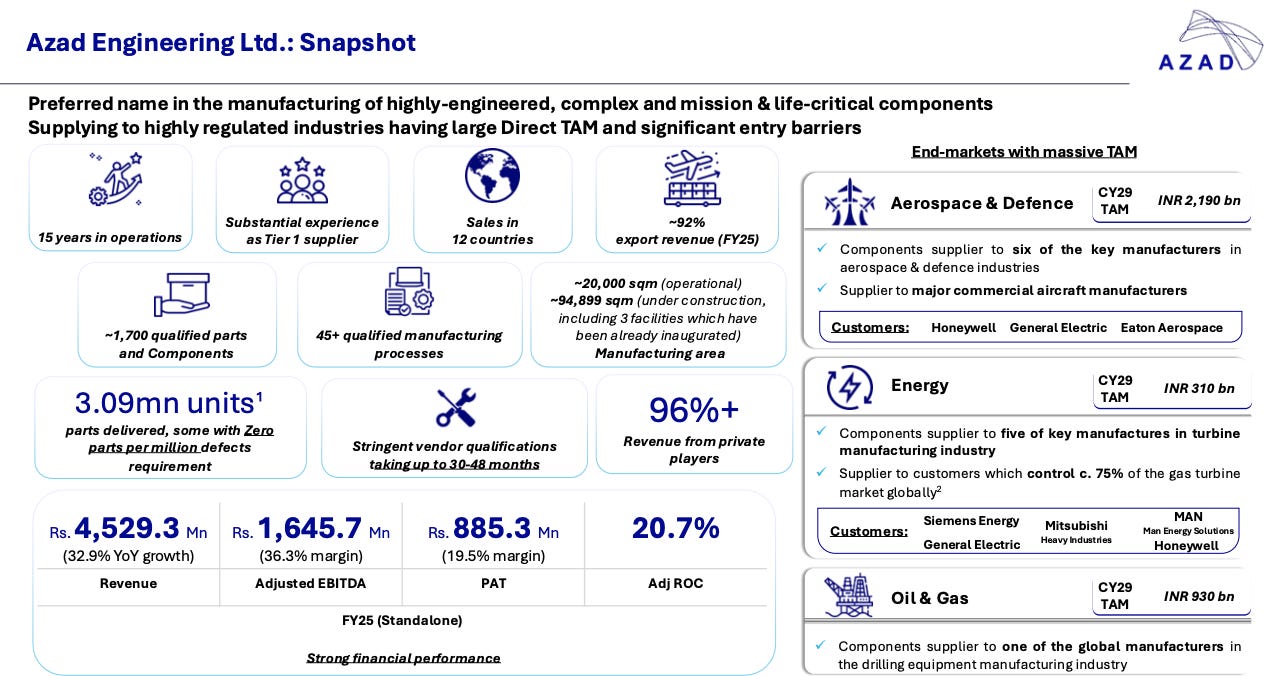

Azad Engineering is a Hyderabad based manufacturer of precision forged and machined components that go inside some of the most demanding machines on earth: gas turbines, aircraft engines, nuclear turbines, and oil and gas drilling rigs. What this means in plain terms is that Azad makes the individual rotating and stationary blades, airfoils, nozzle vanes, and critical sub components that sit inside these machines, spinning at extreme speeds, under extreme temperatures, where any dimensional error or material flaw would be catastrophic. These are not standard off-the-shelf parts. They are one-of-a-kind, customer-specific, made to tolerances measured in micrometers.

What Azad Engineering Does

The company was started in 2008 by Rakesh Chopdar, a high school dropout who had spent 12 years working in his father’s small nuts and bolts factory in Hyderabad. He began with a single second hand CNC machine in a rented shed, and his first significant customer was a government owned power equipment manufacturer that needed turbine airfoils. From there, he progressively moved into harder, more technically demanding parts - first for energy turbines, then for aerospace, then for defense. The company has been incorporated since 1983 (as Azad Engineering Private Limited) but the current precision engineering business was effectively built from 2008 onwards when Chopdar set up the CNC machining operation.

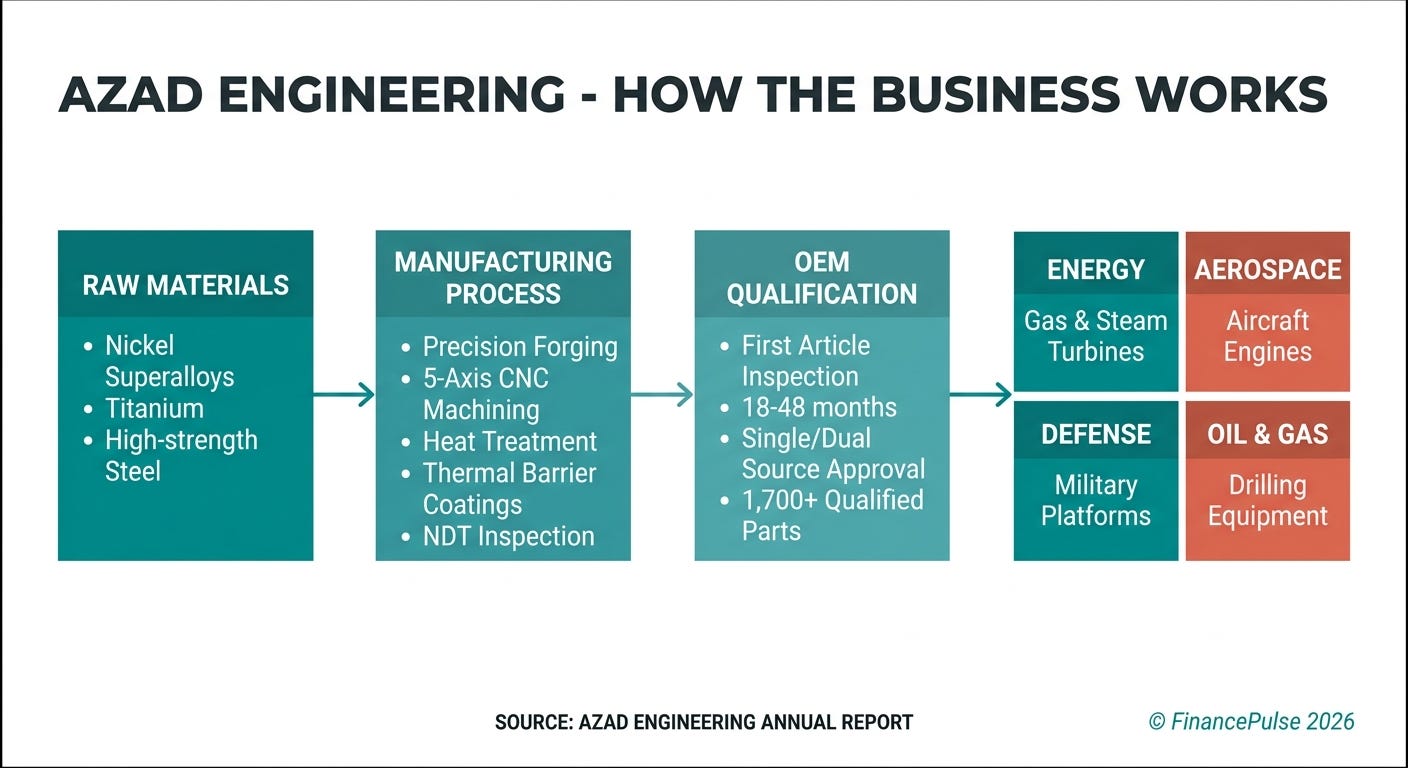

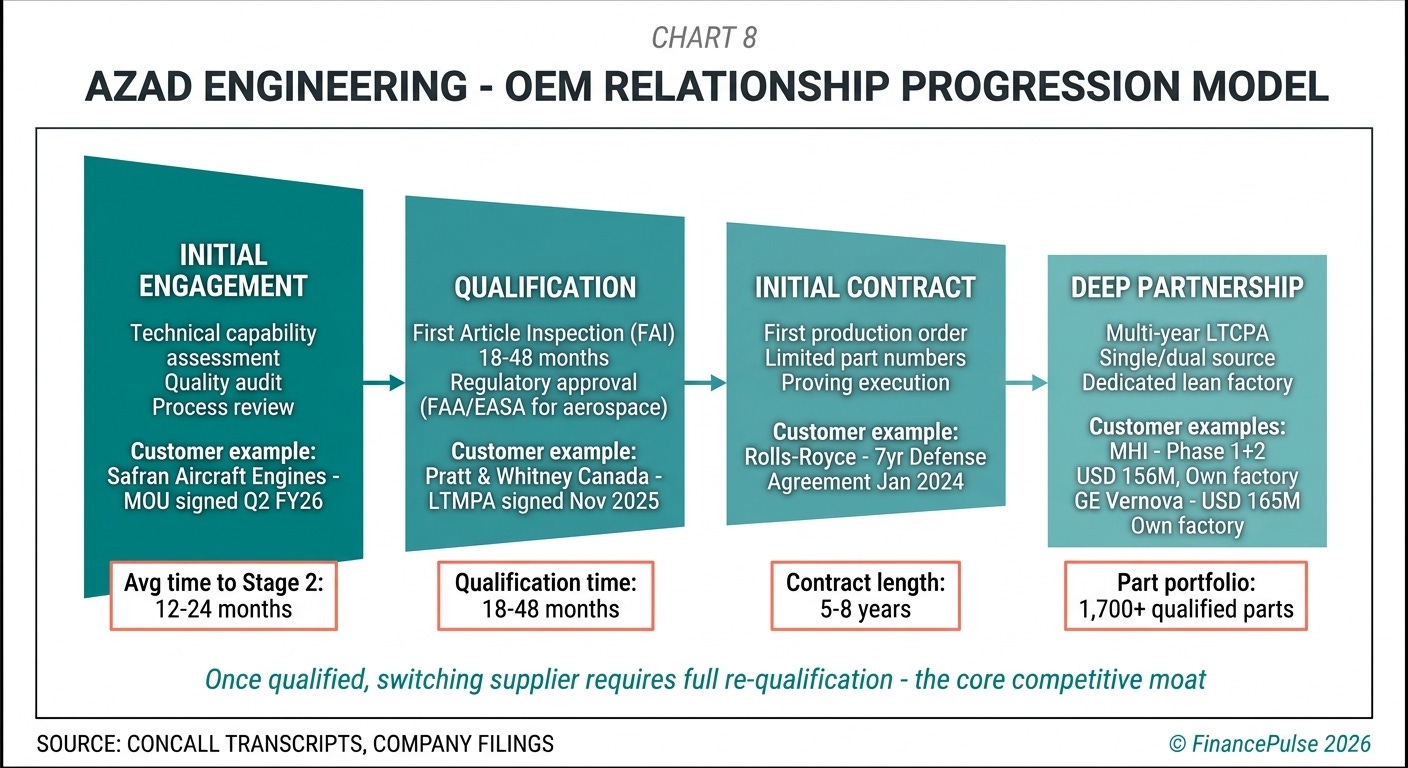

Azad operates at a point in the global supply chain where the product is too technically complex for low-cost manufacturers to produce and too cost sensitive for OEMs to make in house. Turbine blades are manufactured through a multi step process that involves precision forging of difficult alloys like nickel superalloys and titanium, followed by complex 5-axis CNC machining, heat treatment, and specialized coatings - all to sub-millimeter tolerances. The customer then runs these parts through a qualification process lasting anywhere from 18 to 48 months before they are approved for production. Once qualified, Azad becomes the single source or dual-source supplier for that part for the duration of a long-term contract, typically 5 to 8 years.

The sticky point is not just technical skill - it is the qualification itself. A turbine blade used in a GE Vernova gas turbine that powers a data center cannot be switched to a different supplier without re-running the entire qualification, re-certifying every process, and spending 2-4 years doing it again. This means that once Azad wins a part qualification, it essentially owns that part number for the life of the contract. With over 1,700 qualified parts and 45+ manufacturing processes, the cumulative barrier Azad has built is the reason why it calls itself the only Indian company qualified to make these products to global OEM standards.

Exports account for approximately 92% of revenue (Q1 FY26). Customers span the USA, Europe, Japan, and the Middle East. Azad describes its relationship as “trusted Tier 1 supplier” to global OEMs - meaning it supplies directly to the OEM, not through a Tier 2 intermediary.

Business Segments

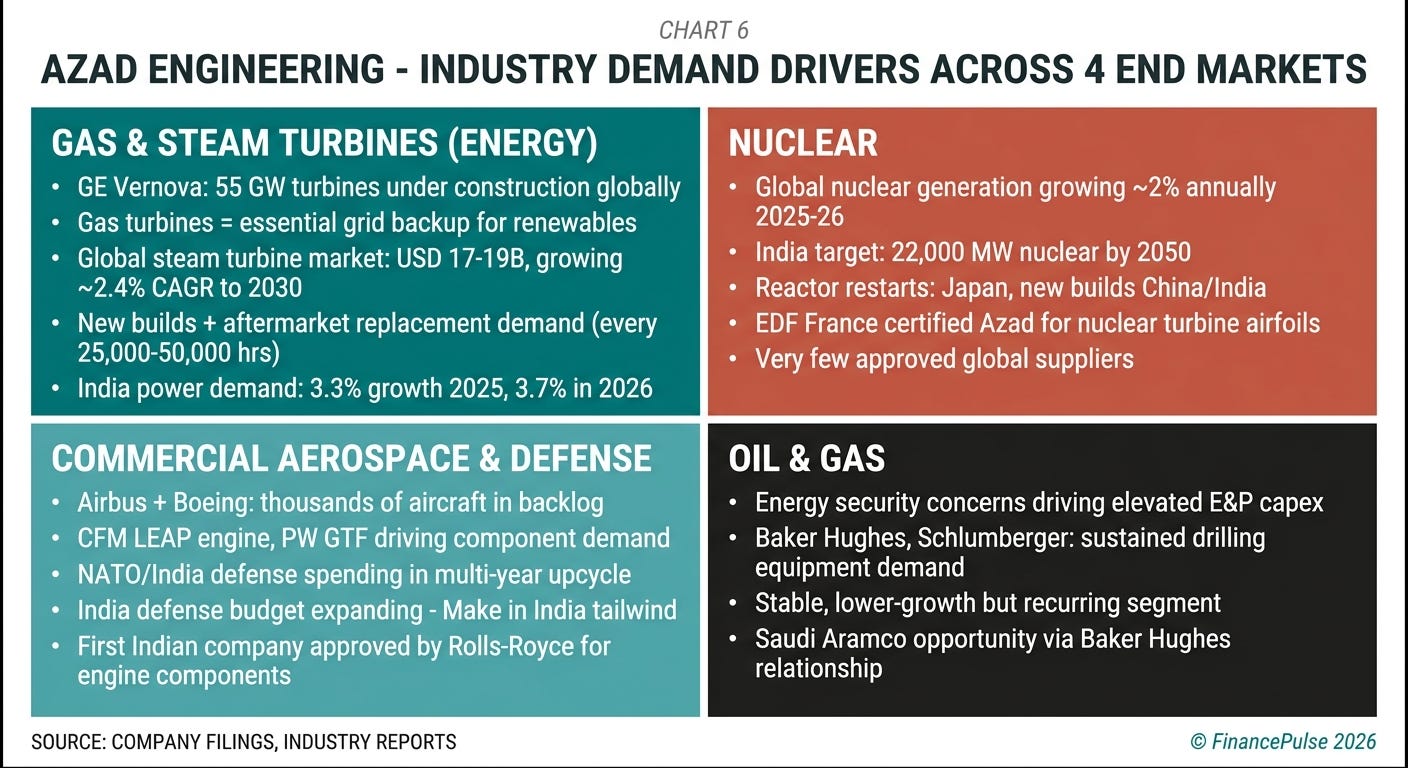

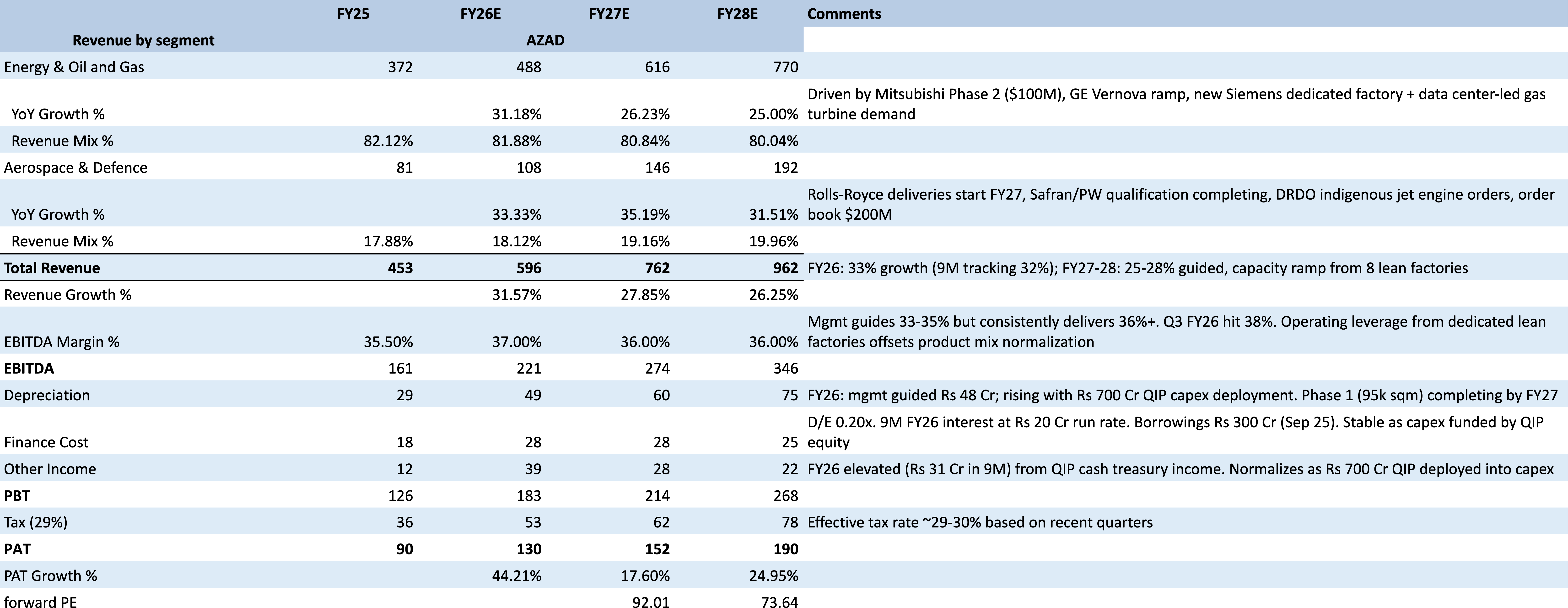

Energy

Energy is Azad’s largest and most established segment, contributing approximately 81% of quarterly revenue as of Q2 FY26. The energy segment covers gas turbines, steam turbines, thermal turbines, and nuclear turbines. Within this segment, Azad manufactures the hot section rotating and stationary airfoils - specifically the blades, vanes, and nozzle segments that direct and accelerate high temperature combustion gases through the turbine stages.

The core capability is the ability to machine nickel based superalloys to aerospace-grade tolerances under conditions that simulate the thermal and mechanical stress the part will experience in operation. A gas turbine blade operates at temperatures that can exceed the melting point of the base metal - which is only possible because of sophisticated cooling channel designs drilled inside the blade and thermal barrier coatings applied to the surface. Azad makes the blade itself; the precision of the cooling holes and the geometry of the airfoil profile are what make or break turbine efficiency.

Azad’s energy customers read like a who’s who of global turbine manufacturing: Mitsubishi Heavy Industries (MHI), Siemens Energy, GE Vernova, Baker Hughes (through subsidiary Nuovo Pignone), Arabelle Solutions, and BHEL. The company has dedicated lean manufacturing facilities for both MHI (inaugurated March 2025, 7,200 sq m at Tunikibollaram, Hyderabad) and GE Vernova (inaugurated April 2025, 7,600 sq m). These customer dedicated plants are a notable feature - rather than running a general-purpose job shop, Azad builds a manufacturing cell specifically optimized for a single customer’s parts, with workflow, tooling, and processes designed around that customer’s specifications.

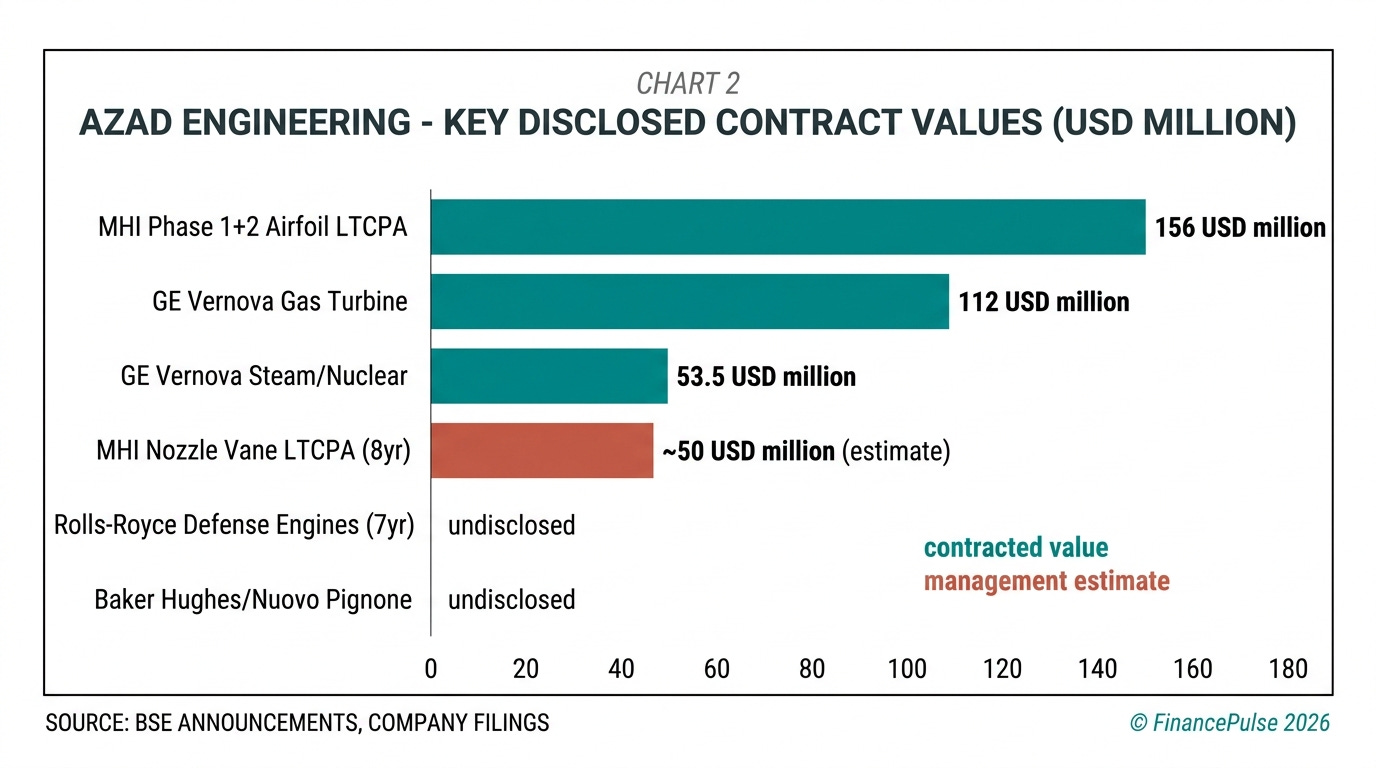

Azad signed Phase 1 of a long-term contract and price agreement (LTCPA) with MHI in November 2024 for supply of rotating and stationary airfoils for gas and thermal power turbines. Phase 2 followed in September 2025. The combined contract value across both phases is USD 156.36 million (approximately Rs 1,387 crore). In addition to this, Azad signed an 8-year LTCPA with MHI in March 2026 as a single source supplier for hot-section nozzle vane segments. MHI also awarded Azad the “2024 Partner of the Year” award, selected from over 1,000 global partners.

With GE Vernova, Azad signed a 6-year supply agreement in January 2025 for USD 112 million (Rs 960 crore) for gas turbine airfoils, and a separate 6-year agreement in May 2025 with GE Vernova’s steam power services for USD 53.5 million (Rs 458 crore) covering nuclear and thermal power airfoils.

The market dynamics for energy are driven by two forces: the global gas turbine backlog, and nuclear’s revival. GE Vernova alone has 55 GW of turbines under construction globally as of the 2025 annual report. Gas turbines are the swing capacity in grids transitioning to renewables - they can ramp up and down fast, which intermittent solar and wind cannot do. Global electricity demand is projected at 3.3% growth in 2025 and 3.7% in 2026, and gas turbines remain indispensable for dispatchable power. This creates a sustained demand pull for Azad’s turbine components.

On nuclear, India targets 22,000 MW of nuclear capacity by 2050. Globally, nuclear generation is set to grow by nearly 2% annually in 2025-26. Azad has qualified for nuclear turbine airfoils and was recently certified to supply nuclear turbine components to EDF France.

Aerospace and Defense

Aerospace and defense is the faster growing, higher margin segment, contributing approximately 19% of revenue as of Q2 FY26, but growing at 30.3% YOY in H1 FY26 versus 35.7% for energy - the aerospace ramp is progressing and management describes it as “the next wave.”

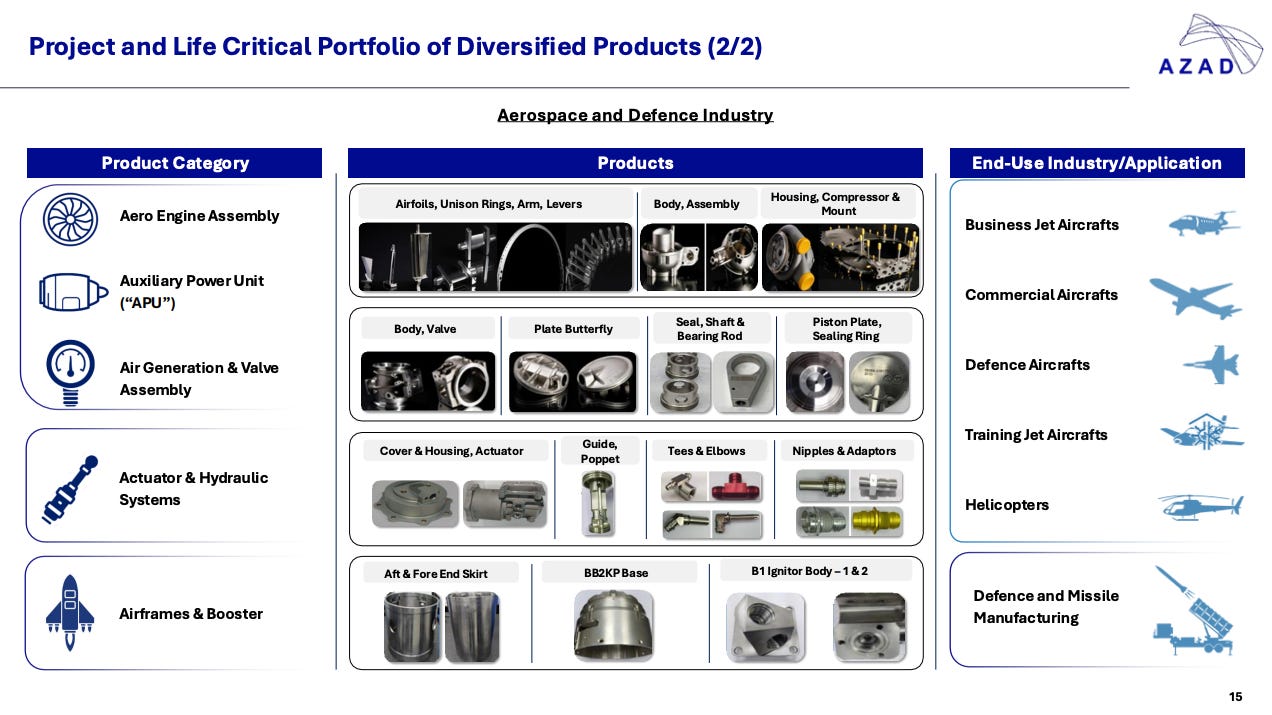

In aerospace, Azad makes rotating airfoils for aircraft engines (3D blades and vanes used in jet engines), as well as hydraulic system components, actuators, and fluid distribution parts for aircraft. The company’s aerospace portfolio supports platforms including the Boeing 737 and 747 families, Airbus A320, A350, Boeing 777, and Gulfstream G550. These are not low complexity stampings - they are the blades inside CFM56 and similar engines, and the structural hydraulic components that move the flight control surfaces.

The defense side includes components for military aircraft, missiles, and defense platforms. Azad manufactures components for Russian origin platforms (the Sukhoi Su-30MKI fighter used by the Indian Air Force has some Azad components) as well as for BrahMos (the supersonic cruise missile). The company has also secured a contract from India’s Ministry of Defence to serve as a production agency for the Gas Turbine Research Establishment’s (GTRE) Advanced Gas Turbine Engine (AGTE) - a long term contract to manufacture and assemble complete turbine engines for the Kaveri program, marine gas turbines, and army gas turbines.

The OEM relationships in aerospace are the deepest moat Azad has in this segment. Rolls Royce signed a 7 year agreement with Azad in January 2024 for components for defense aircraft engines - this was the first time an Indian company was approved by Rolls-Royce for complex engine components, and it opened the entire Rolls-Royce supply chain for Azad. Safran Aircraft Engines signed an MOU with Azad in Q2 FY26 for critical rotating engine components for defense platforms - the first step in what Azad describes as the same progression it went through with Rolls-Royce: MOU, technical assessment, qualification, contract. Pratt & Whitney Canada signed a long-term Master Terms and Purchase Agreement with Azad in November 2025 for aircraft engine components. Honeywell Aerospace and GE Aerospace are also in the customer list.

Azad VTC Private Limited, the subsidiary, received NADCAP accreditation for coatings in Q2 FY26 - this is a critical aerospace quality certification that validates Azad’s thermal barrier and other coating capabilities to international standards.

Oil and Gas

Oil and gas is the smallest segment but has stable, recurring demand. Azad manufactures components for drilling rigs - drill bits, slips used in wellhead and downhole equipment, reamers, and other precision parts used in exploration and production. Customers include Baker Hughes, and Azad has signed a 5-year strategic supply contract amendment with Nuovo Pignone (a Baker Hughes subsidiary) in May 2025, extending an existing agreement.

The oil and gas segment benefits from the same precision machining infrastructure as energy and aerospace. The parts are less technically demanding than hot section turbine airfoils, but require tight tolerances and materials that withstand downhole pressures and corrosive environments.

Azad also has a presence in the standalone power supply (SPS) segment, which covers small, portable power generation units used in military and remote applications - these require compact gas turbines, and Azad supplies components to these OEMs as well.

Products and Business Detail

Azad’s product catalogue is organized around three types of parts across four end markets:

Rotating airfoils - these are the 3D blades in both compressor and turbine stages of gas, steam, and aircraft engines. Compressor blades are made from titanium and high-strength steel alloys; turbine blades are made from nickel superalloys with complex internal cooling geometries. The turbine blades are the highest value, most demanding products Azad makes. A single gas turbine can have hundreds of blades across multiple stages, each made to different specifications.

Stationary airfoils (nozzles and vanes) - these are the fixed components that direct gas flow onto the rotating blades. They operate at even higher temperatures than rotating blades because the combustion gases hit them first. The hot section nozzle vane segments in Azad’s March 2026 MHI contract are among the most technically demanding components they make.

Hydraulic and fluid distribution components - for aerospace, these are the manifolds, fittings, and structural parts that carry hydraulic fluid through the aircraft’s flight control and actuation systems. Azad makes these from forgings (aluminum, titanium, stainless steel) to tight dimensional tolerances with internally machined passages.

Drill bits and downhole tools - For oil and gas, polycrystalline diamond compact (PDC) drill bits and other cutting tools used in oil and gas exploration drilling.

Manufacturing process: A typical blade starts as a raw investment casting or forging blank sourced from specialized suppliers (this is where the qualification pain begins - Azad must pre-qualify these input suppliers with the OEM, which adds to qualification lead time and working capital). The blank is then fixtured on a 5-axis CNC machining center and machined to final dimensional specifications. This involves removing material from complex curved 3D surfaces while holding tolerances of +/- 0.02mm or tighter. After machining, the part goes through heat treatment, non-destructive testing (fluorescent penetrant inspection, X-ray, ultrasound depending on the part), and final dimensional inspection. Some parts receive thermal barrier coatings applied by plasma spray or air plasma spray processes in Azad’s coatings subsidiary.

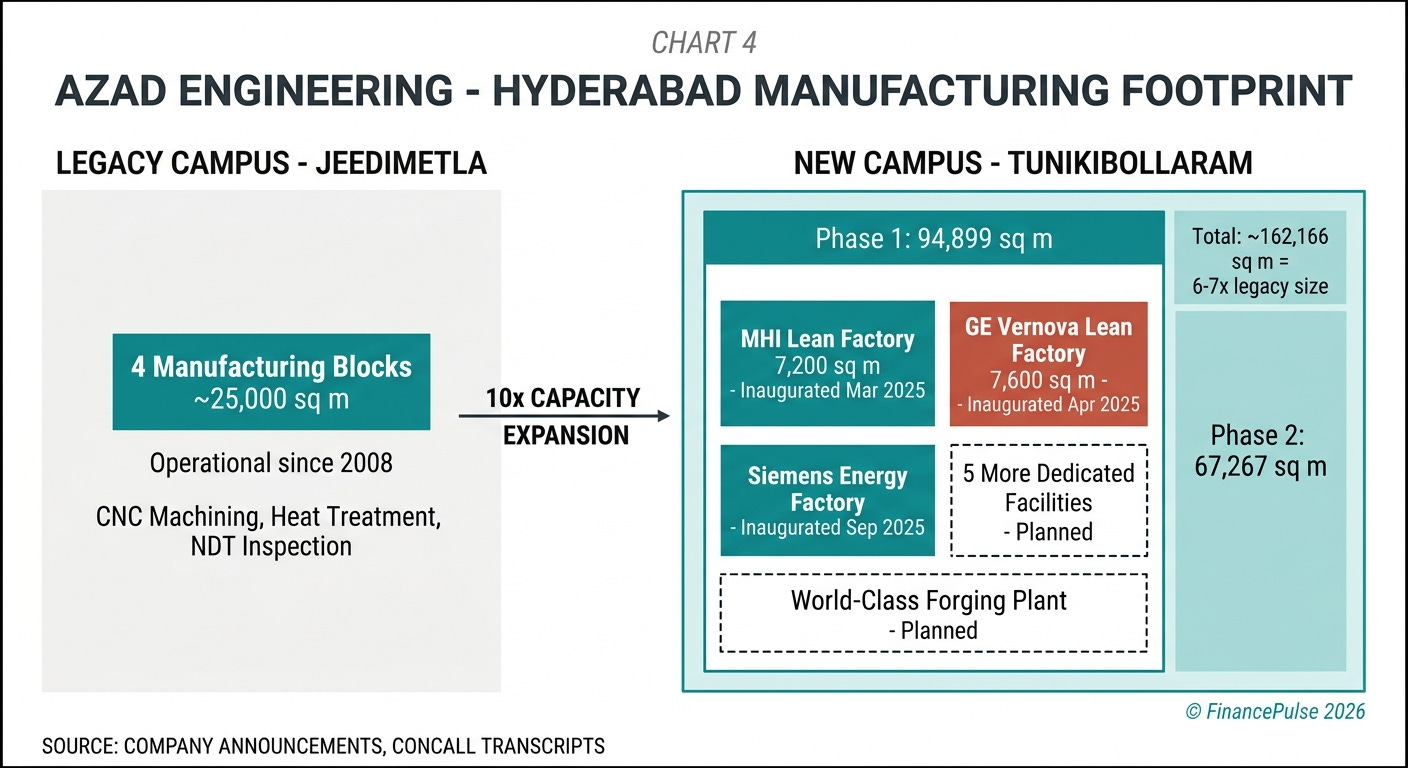

Facilities: Azad currently operates four manufacturing blocks at its legacy facility in Jeedimetla, Hyderabad, covering approximately 20,000-25,000 sq m. Since the IPO, it has commenced a 10x capacity expansion at Tunikibollaram, Hyderabad. Phase 1 covers 94,899 sq m and Phase 2 covers 67,267 sq m - together this new campus is approximately 7-9x the existing footprint. Within the new campus, Azad is building customer-dedicated lean manufacturing cells: the MHI lean factory (7,200 sq m, inaugurated March 2025), the GE Vernova lean factory (7,600 sq m, inaugurated April 2025), with plans for 8 such dedicated facilities total including a state-of-the-art forging plant.

Azad also acquired the assets of VTC Surface Technologies in May 2024 - a company specializing in advanced wear, corrosion, and heat resistant coatings. This brings critical coating capability in-house. The subsidiary (Azad VTC Private Limited) has since achieved NADCAP accreditation for aerospace coatings.

Certifications held: ISO 9001:2015, AS 9100:2016 (aerospace quality management), NADCAP (special processes, coatings), and various OEM-specific approvals from GE, Siemens, MHI, Rolls-Royce, and others. Each OEM has its own supplier qualification process that runs separately from the standard certifications.

Geographies: over 92% export revenue. Customer countries include the USA, Japan, Germany, France, and the UK. Azad also has an MOU to establish a manufacturing presence in Saudi Arabia, explored through its relationship with Baker Hughes - the Saudi energy market (Saudi Aramco and others) presents a potential geographic expansion opportunity.

Customers

The buying relationship at Azad is unusual because the customer is not just buying a part - they are qualifying a supplier. When GE Vernova decides to source turbine blades from Azad, it is making a multi-year commitment. The process starts with a technical assessment of Azad’s manufacturing capabilities, quality systems, and process control. It then moves to a First Article Inspection (FAI) where Azad produces sample parts that are measured and tested against every requirement. Only after FAI approval does the OEM place a production order. The entire process can take 18 to 48 months. For aerospace, add another layer: the FAA or EASA (European Aviation Safety Agency) may also need to approve the part design change before Azad’s production parts can fly.

Once this qualification is complete, switching to a different supplier requires starting the entire process again. This is why Azad’s attrition in the customer base is effectively zero - no OEM voluntarily goes through a 2-4 year requalification to switch suppliers, especially for life-critical parts. Rakesh Chopdar described it in the Q2 FY25 concall: “We are the only one in the country for certain product line. There is no one else.”

The customer base is concentrated but the concentration is by design. Azad targets the top 5-6 global OEMs in each end market and aims to grow wallet share within those relationships. As of Q2 FY26, management noted that their wallet share across customers in energy, aerospace, defense, and oil and gas is approximately 1-1.5% - which means there is substantial room to grow revenue within existing customers without winning a single new OEM relationship. Every time Azad qualifies a new part within a customer relationship, it adds to the locked-in revenue base.

Key customers as disclosed or confirmed: Mitsubishi Heavy Industries (largest disclosed relationship - combined contracts worth USD 156 million+), GE Vernova (gas turbine and steam power divisions - combined contracts USD 165 million+), Siemens Energy, Rolls-Royce (7-year defense engine deal), Safran Aircraft Engines (MOU stage), Pratt & Whitney Canada, Baker Hughes/Nuovo Pignone, Honeywell Aerospace, Arabelle Solutions (a subsidiary of GE), BHEL, and GTRE/DRDO for the Indian defense segment.

Average customer relationship is over 10 years for key accounts. The MHI relationship began in 2012. The GE relationship has been in place since the early days. This longevity matters because the OEM’s engineering team has already embedded Azad’s part drawings into their product lifecycle documentation - any change requires a formal engineering change order.

Azad primarily operates on long-term contract and price agreements (LTCPAs), typically 5-8 years in duration with fixed pricing (often with annual escalation clauses for raw material and labor indices). This provides revenue visibility but also means Azad bears the raw material price risk in the intervening period if contracts don’t have adequate pass through provisions.

Competitive Landscape

The global market for high-precision turbine airfoils and aerospace components is not a crowded one. Azad competes in two different competitive arenas.

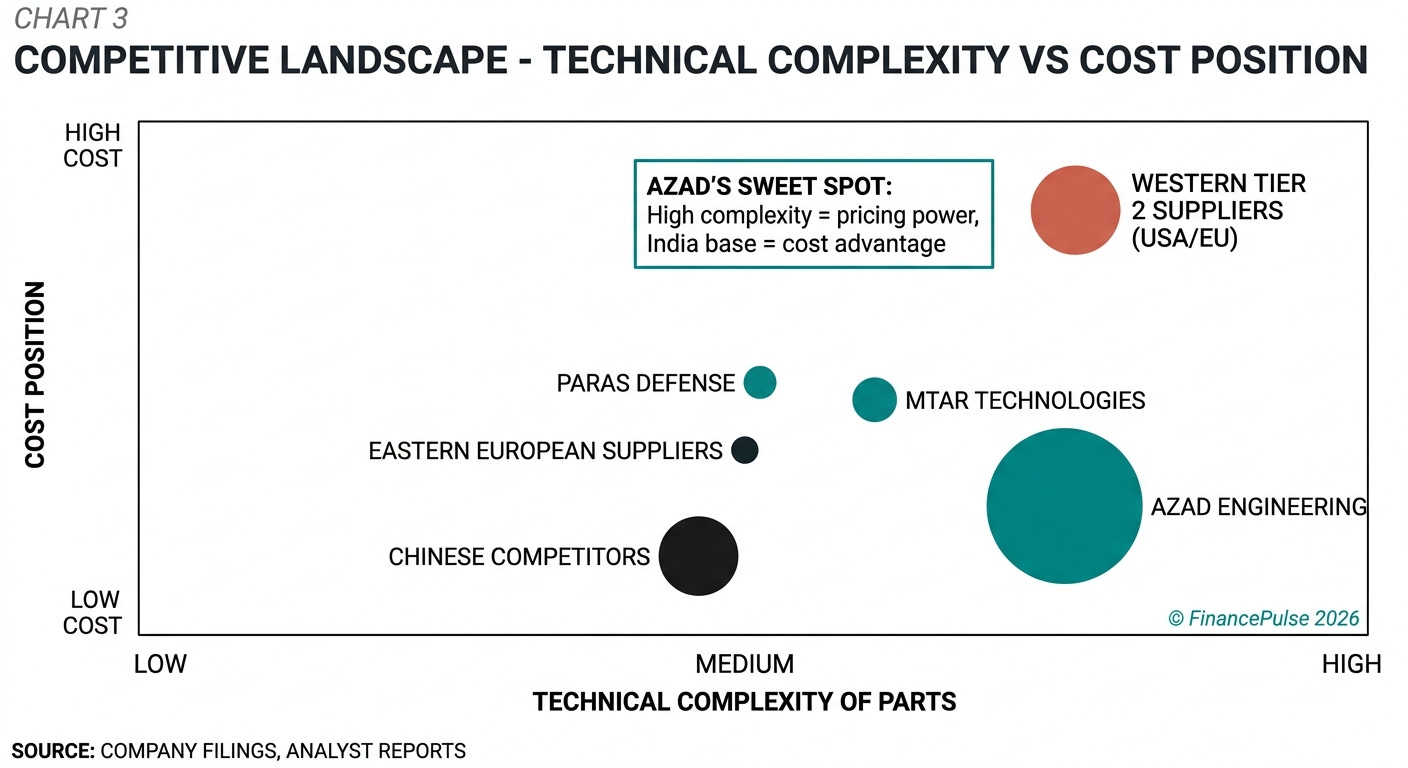

Global competition: In the energy turbine components segment, Azad’s global competitors are primarily in China (Baoji Titanium Industry, Deyang Heavy Industry), Eastern Europe (Czech, Slovak, and Polish precision component companies), and Southeast Asia (Singapore and Thailand-based shops). The company’s annual report explicitly notes “growing competition from China and Eastern Europe.” Chinese competitors in particular can offer lower prices for simpler components. However, for hot-section components - the rotating airfoils in the highest-temperature stages of a gas turbine - Chinese suppliers have struggled to achieve OEM qualifications from GE, Siemens, and MHI because the process knowledge and metallurgical expertise required are extremely hard to replicate quickly. Azad’s 15+ years of building this knowledge base is the core competitive advantage.

In aerospace, global competitors include Tier 2 precision component suppliers from the USA (Honeywell Aerospace has in-house manufacturing, GE has some self-manufacture, but the Tier 2 supply chain includes companies like Heico, Transdigm subsidiaries, and Europe-based specialists), UK (Rolls-Royce’s own supply chain), France (Safran’s supply chain), and increasingly India.

Indian competition: Within India, the closest comparables in the precision components space are MTAR Technologies (makes critical components for nuclear, space, defense, and clean energy - FY26 Q3 revenue of Rs 278 crore), Paras Defense (primarily defense-focused, order book of Rs 1,100 crore), PTC Industries (aerospace castings), and Dynamatic Technologies (hydraulics and aerospace). The key differentiator is Azad’s margin profile - it has the highest operating margins among Indian peers because it targets the most technically demanding, highest-value products. Where MTAR and Paras make components for the Indian defense ecosystem (ISRO, DRDO, HAL), Azad makes components that go directly into commercial global OEM products - which means its revenue is dollar-denominated, pricing is set by global market dynamics, and the customer base is far more commercially rigorous.

Unimech Aerospace is another Indian peer in precision tooling for aerospace, but operates in a different niche (tooling vs. actual flight components).

Barriers to entry: the qualification process is the single most powerful barrier. Building the physical manufacturing capability (CNC machines, forge shop, heat treatment, inspection labs) requires Rs 500 crore+ in capital. Beyond the physical capability, earning the first OEM qualification takes 2-4 years. And the first qualification only unlocks one part number - building a 1,700-part portfolio takes decades. An entrant starting today would not be a credible alternative to Azad for existing OEM contracts for at least 7-10 years.

There is also a process knowledge barrier that money cannot easily replicate. Knowing how to machine a nickel superalloy at high metal removal rates without introducing residual stresses that cause fatigue cracking in operation - this is learned through years of trial, failure, and refinement on real production programs. Azad has built this tacit knowledge base over 15 years.

Why Azad wins: (1) It is already qualified - the entry barrier is behind it, not ahead of it; (2) it operates from India, giving it a structural cost advantage of 20-30% versus western competitors who make similar components; (3) its quality record (4+ million zero-defect components delivered since inception) gives OEMs confidence that the cost advantage doesn’t come with quality risk; (4) single-source positioning on most part numbers means price competition is limited once a relationship is established; (5) the “China+1” supply chain shift is structurally benefiting India as a manufacturing destination, and Azad is positioned directly in the path of that shift.

Where Azad could lose: (1) If Chinese suppliers accelerate OEM qualifications in western markets, particularly in the energy segment; (2) if Azad misexecutes on its 10x capacity expansion - delivering late or with quality issues during ramp-up could damage relationships; (3) if key customer relationships are concentrated and one large OEM reduces its sourcing from Azad.

Industry

Gas turbines: the global gas turbine market is driven by the insatiable demand for dispatchable power. Despite the growth of solar and wind, electricity grids need backup capacity that can switch on in minutes when the sun stops shining or the wind drops. Gas turbines fulfill this role. GE Vernova alone has 55 GW of turbines under construction globally - a backlog that will take several years to deliver, and each of those turbines needs thousands of precisely manufactured blades and vanes. The global steam turbine market was valued at USD 17-19 billion in 2024 and is expected to grow at approximately 2.4-2.5% CAGR through 2030.

Beyond new builds, the installed base of gas turbines requires regular maintenance and component replacement. Turbine blades have finite lifespans and must be replaced at maintenance intervals (typically every 25,000-50,000 operating hours). This creates a large, recurring aftermarket demand on top of the new build market. Azad participates in both new build and aftermarket supply.

Nuclear: global nuclear generation is growing at nearly 2% annually in 2025-26, supported by reactor restarts in Japan, new builds in China and India, and the revival of nuclear as a policy tool for decarbonization in Europe and the USA. India has committed to 22,000 MW of nuclear capacity by 2050 - which requires a vast supply of turbine components for the steam turbines that convert reactor heat into electricity. Azad’s qualification for nuclear turbine airfoils, including its certification by EDF France, positions it in a segment that has very few approved suppliers globally.

Aerospace: Commercial aviation is recovering from the COVID collapse. Airbus and Boeing have backlogs of thousands of aircraft, and both are trying to accelerate delivery rates. The CFM International LEAP engine (which powers the A320neo and 737 MAX) and Pratt & Whitney’s geared turbofan are the dominant new-generation engines, and the supply chains for these engines need to scale up. Azad’s qualifications on Rolls-Royce, Pratt & Whitney, and Safran programs position it directly in the path of this ramp-up.

Defense aerospace globally is in an expansion phase driven by the Russia-Ukraine conflict reshaping European defense spending, increasing India’s defense budget, and NATO partners re-arming. This creates demand for military aircraft engines, missiles, and naval gas turbines.

Oil and gas: oil and gas exploration CAPEX remains elevated as energy security concerns drive investment in domestic production. Baker Hughes, Schlumberger, and Halliburton continue to manufacture drilling equipment that requires precision components. This is a stable, lower-growth segment for Azad.

India’s aerospace ecosystem: the Indian government’s Make in India and Aatmanirbhar Bharat policies are creating a policy tailwind for domestic aerospace manufacturers. The Ministry of Defence has issued “positive indigenization lists” requiring domestic procurement for specified defense systems. The GTRE contract to manufacture the Kaveri-derived AGTE engine is a direct result of this policy. The India-USA defense technology cooperation framework and India’s engagement with France (on Rafale follow-ons and Sukhoi upgrades) are also creating opportunities for Indian precision component makers in global defense supply chains.

Growth Triggers

MHI Phase 1 and Phase 2 contracts ramp-up: The combined USD 156 million MHI contract is in the early stages of production. The dedicated 7,200 sq m facility inaugurated in March 2025 is currently employing 200 workers and is expected to scale. Management on the Q2 FY26 call: “With the combined contract value with MHI now stands at INR 1,387 crores, a strong testament to our technical excellence.”

GE Vernova ramp-up across two contracts: the USD 112 million gas turbine contract and the USD 53.5 million steam/nuclear power services contract run for 6 years each, with revenue building as production capacity ramps in the dedicated GE Vernova factory inaugurated April 2025. “The facility was inaugurated in the presence of Siemens Energy”s senior global leadership team” (BSE filing, Sep 2025, describing the Siemens lean factory).

10x capacity expansion commissioning: “In the next 12 to 18 months, we plan to have a total 8 dedicated lean manufacturing facilities, including 1 state of art, world-class forging plant at Tunikibollaram, Hyderabad.” The new facility will be approximately 5-6 lakh square feet, versus the current ~25,000 sq m. As this capacity comes online, Azad can fulfill orders it currently has capacity constraints on.

Wallet share expansion within existing OEMs: Rakesh Chopdar: “Our wallet share as it... which is what products Azad is related to is around 30 billion plus. This is just a start.” Azad currently captures approximately 1-1.5% of its addressable wallet share across customers. As new qualifications complete and capacity comes online, this percentage grows.

Pratt & Whitney Canada long-term agreement: the long-term Master Terms and Purchase Agreement signed in November 2025 opens the Pratt & Whitney Canada supply chain - a significant new relationship in aircraft engines. “The partnership sets the stage for a deeper strategic collaboration, giving Azad a stronger foothold in the global aerospace supply chain.”

Safran MOU - aerospace qualification pipeline: the Safran MOU signed in Q2 FY26 for critical rotating engine components for defense platforms. Murali Krishna (Managing Director) on the call: “This agreement sets the framework for cooperation in developing critical rotating engine components for strategic defence platforms. This is an important step forward in strengthening India’s aerospace ecosystem.” Per the pattern with Rolls-Royce (MOU, then technical assessment, then 7-year contract), the Safran MOU could convert to a long-term supply agreement within 2-4 years.

DRDO AGTE engine production: Azad secured a contract from India’s Ministry of Defence to be the production agency for the Advanced Gas Turbine Engine designed by GTRE. This is a qualitatively different kind of contract - it is not a component supply agreement but a production agency contract for complete engines. First deliveries were targeted for early 2026.

Saudi Arabia facility: “We are now planning to set up a shop in Saudi Arabia... When we met the Ministry of Energy, we met their clients, they took us to their clients, which is Saudi Aramco and many more companies.” A manufacturing presence in Saudi Arabia, enabled through the Baker Hughes relationship, would open the Middle East market for Azad and reduce logistics costs for a large energy market.

MHI 8-year single-source nozzle vane contract: Azad signed an 8-year LTCPA with MHI as the single-source supplier for hot-section nozzle vane segments - one of the most technically demanding components in a gas turbine. This adds a new, long-duration revenue stream on top of the existing MHI airfoil contracts.

Coatings capability and NADCAP accreditation: Vishnu Malpani (Whole-time Director): “Azad VTC Private Limited, our subsidiary has achieved NADCAP accreditation for coatings.” This unlocks the ability to apply aerospace-grade coatings in-house for aerospace customers, a critical step toward capturing more of the value chain on each part.

Key Risks

Capacity ramp-up execution risk: the 10x expansion is Azad’s defining bet. Building 5-6 lakh sq ft of manufacturing space, equipping it with specialized CNC machinery that takes 6-18 months to deliver from German and Japanese machine tool manufacturers, hiring and training specialized machinists, and running OEM qualification audits on the new facility - all simultaneously - is operationally complex. Management acknowledged in the Q1 FY26 concall (August 2025): “It has been challenging to match the growing demand with our facility to ramp up. We anticipate to similarly address these challenges to continue for a couple of upcoming quarters.” A delay in commissioning translates directly to revenue deferral.

Working capital intensity: Azad requires high inventory to support the qualification process. Before a part is approved, Azad must run a full qualification batch - which requires purchasing the minimum order quantity of raw castings or forgings from the OEM-approved sub-supplier (e.g., 500 castings to qualify 5 pieces). This inventory sits until qualifications are complete. Rakesh Chopdar in the Q2 FY25 concall: “As the qualification is done, then that is done... The taper off is coming... That is just coming out of this phase.” The business had 179 days of debtors as of recent data, and the working capital cycle was a consistent point of analyst focus. As the company scales, the absolute working capital required grows. The QIP proceeds (Rs 700 crore raised in Feb/March 2025) provide a buffer, but sustained growth will require continued working capital funding.

Raw material price risk: Azad uses nickel superalloys, titanium, and specialized steel alloys whose prices are globally determined and volatile. The company operates on long-term fixed-price contracts with OEMs (with some escalation clauses), meaning sharp moves in nickel or titanium prices compress margins unless fully hedged or passed through. This is exactly what happened in Q3 FY26: management noted on the Q3 FY26 concall that margins were impacted because the company was buying raw materials at spot rates (no long-term contracts in place) as it transitioned to self-sourcing through newly commissioned backward integration assets.

Customer concentration: while the OEM relationships are deep and sticky, the revenue base is likely concentrated among 2-3 major customers. Any slowdown in CAPEX at MHI or GE Vernova, any shift in their sourcing strategy, or any quality issue that triggers a supplier review, would have an outsized impact on Azad’s revenue.

Qualification failure or delay risk: Azad’s growth depends on completing new part qualifications that unlock production contracts. The qualification process is not within Azad’s full control - the OEM’s engineering and quality team must sign off. Delays in OEM qualification timelines (OEMs reducing their own engineering bandwidth, changing product designs mid-qualification) can push revenue out by quarters.

Currency risk: with over 90% of revenue in foreign currency (USD, EUR, JPY) and cost base in Indian Rupees, the company benefits from Rupee depreciation and is hurt by Rupee appreciation. Management mentioned FX as a margin variable in multiple concalls.

Single-promoter risk: Rakesh Chopdar is the founder, chairman, and CEO simultaneously. The business’s deep OEM relationships, technical knowledge navigation, and strategic decisions are concentrated in one individual. Succession and key-person risk is a legitimate concern for a company with this degree of founder-dependence.

Scenarios & Valuations

Bull Case

The new manufacturing campus at Tunikibollaram commissions fully by end of FY27 and reaches peak utilization by FY28 as guided. The eight dedicated lean factories become fully operational, each running at high utilization for a specific OEM customer. The Safran MOU converts to a long-term supply agreement within 2-3 years, adding a major French aerospace engine maker to the customer base - this is particularly significant because Safran’s CFM International joint venture (with GE) makes the LEAP engine that powers every Airbus A320neo, the best-selling commercial aircraft in history. The Pratt & Whitney Canada relationship deepens from the initial master agreement into substantial production volumes. The DRDO AGTE engine production begins generating meaningful revenue as Indian defense modernization accelerates. The Saudi Arabia facility opens, reducing logistics friction for Middle Eastern customers and adding a new manufacturing hub.

In this scenario, the combination of existing OEM relationships growing wallet share, new OEM relationships converting from MOU to contract, and the 10x manufacturing capacity coming online creates a flywheel: more capacity enables more qualifications, more qualifications create more locked-in revenue, more locked-in revenue enables more investment. The “China+1” supply chain shift and India’s defense indigenization policy continue to provide favorable winds. The company grows at 30%+ annually for several years and the EBITDA margin expands beyond 35% as operating leverage kicks in on the expanded facility base.

Base Case

The capacity expansion executes broadly on track but faces the normal delays and teething issues of building a complex precision manufacturing facility from scratch. The MHI and GE Vernova facilities ramp up through FY26-27, reaching steady-state by FY28 as management has guided. The Safran relationship progresses through technical assessment but the first production contract is 3-4 years away. Pratt & Whitney Canada generates modest initial volumes as the qualification process completes. The DRDO engine program delivers its first batch on schedule but remains small as a revenue contributor. The Saudi Arabia facility discussions continue but a physical facility is still 2-3 years away.

Revenue growth sustains at 25-30% annually as guided, driven by the existing OEM relationships growing and the new capacity absorbing the backlog. EBITDA margins stay in the 33-35% guided range with some quarterly volatility as new facilities carry startup costs before reaching utilization. Working capital remains elevated during the expansion phase. The order book of Rs 6,500+ crore provides multi-year visibility.

Bear Case

The capacity expansion faces significant delays - machine delivery timelines extend, OEM qualification audits of the new facility identify gaps that require remediation, and key technical staff are difficult to hire in the volumes needed. The new facilities take until FY29-30 to reach meaningful utilization. In the interim, Azad is carrying the CAPEX cost and depreciation of a large, underutilized facility against a revenue base that is growing slowly.

Simultaneously, the raw material cost issue experienced in Q3 FY26 persists - backward integration into self-sourcing is harder than expected, and the company continues buying at spot rates longer than anticipated, compressing margins. One or two large OEM customers slow their own production programs (e.g., GE Vernova faces order cancellations if gas turbine demand softens due to faster-than-expected grid-scale battery storage adoption), reducing the pull on Azad’s capacity. Chinese precision component makers accelerate their OEM qualifications in the energy segment, particularly for less technically demanding turbine stages, putting pressure on Azad’s pricing.

In this scenario, revenue growth slows to 15-20% and margins compress to 28-30% as the fixed cost base from the new facilities creates operating deleverage. The working capital situation worsens as inventory for new qualifications builds while offtake is slower than expected. The 179-day debtor days stretches further, creating cash flow pressure. The company remains fundamentally sound - its existing contracts and qualifications ensure baseline revenue - but the growth story takes several years longer than priced in.

Thanks for reading! Do check out Investorstack.