Beta Drugs

Can Beta Drugs Transform from a Niche Oncology Player into a Global Specialty Pharma Leader?

Before we Begin, Here’s Everything you get with Investorstack subscription:

Research reports

Valuation models (bull/base/bear)

Growth triggers

Read between the lines (concall breakdowns)

KPIs & one-pagers

Scanners

Sector, industry & theme leaderboards

And many more features! For any feedback, reach out on Twitter.

Beta Drugs Limited is an Indian pharmaceutical company that specializes in oncology, specifically the development and manufacture of anti-cancer medicines. The company operates across the entire value chain of oncology pharmaceuticals, from the synthesis of active pharmaceutical ingredients (APIs) to the manufacture of finished dosage forms like injectables, tablets, capsules, and oral suspensions. Founded in 1985 by the late Shri Vijay Batra as part of the Adley Group, the company has transitioned from a small-scale contract manufacturer into an integrated player with its own brand portfolio, a contract development and manufacturing (CDMO) business, an active export division, and specialized divisions in aesthetics and fertility.

The company’s core value proposition lies in making highly complex, expensive cytotoxic cancer therapies affordable and accessible to patients in India and developing international markets. It achieves this through deep backward integration, producing its own active ingredients and intermediates, which insulates it from raw material supply shocks and price volatility. The business model is designed around three main pillars: own branded oncology formulations sold to corporate and government hospitals, CDMO services for major multinational and domestic pharmaceutical companies, and international exports of branded generics and APIs to semi-regulated and regulated markets.

Business Segments

Branded Oncology (Own Brands)

The company’s own branded oncology division is its flagship growth driver, contributing approximately 34% of total revenue as of the first half of Fiscal Year 2026. This division sells branded generic anti-cancer drugs directly to oncology hospitals, private clinics, and government procurement agencies across India. The portfolio spans over 135 oncology products, with a sales team of specialized therapeutic managers covering major medical centers. The branded business has built deep hospital access, covering more than 80% of corporate and government healthcare institutions in the country. A significant milestone was reached in Fiscal Year 2025 when the branded business surpassed ₹100 crore in sales for the first time, compounding at over 25% annually.

CDMO (Contract Development and Manufacturing)

The CDMO segment is the largest division by revenue, contributing approximately 39% of total sales in the first half of Fiscal Year 2026. Beta Drugs is the preferred contract manufacturing partner for cytotoxic oncology products in India, serving more than 49 major domestic and multinational pharmaceutical companies, including Glenmark, Intas, Alkem, Cadila, and Torrent. The company’s dedicated manufacturing facilities in Baddi, Himachal Pradesh, are designed specifically to handle highly hazardous cytotoxic chemicals under strict containment protocols. While the CDMO business provides steady volumes and high utilization, it is subject to product mix variations and occasional margin pressure from low-margin product classes like the platinum group (Cisplatin, Carboplatin, Oxaliplatin), which the company must supply to retain partners.

International Exports

The export division accounts for approximately 21% of total revenue as of the first half of Fiscal Year 2026. The international business is primarily driven by tender-based procurement, meaning sales are seasonal and heavily concentrated in the second half of the fiscal year when global tenders are finalized. The company has built an export network spanning over 46 countries with more than 250 product registrations. Beta Drugs is actively transitioning from unregulated and semi-regulated markets into highly regulated markets. This transition is backed by successful regulatory audits of its facilities by agencies such as COFEPRIS (Mexico) and INVIMA (Colombia), alongside pending approvals for European markets.

Active Pharmaceutical Ingredients (API)

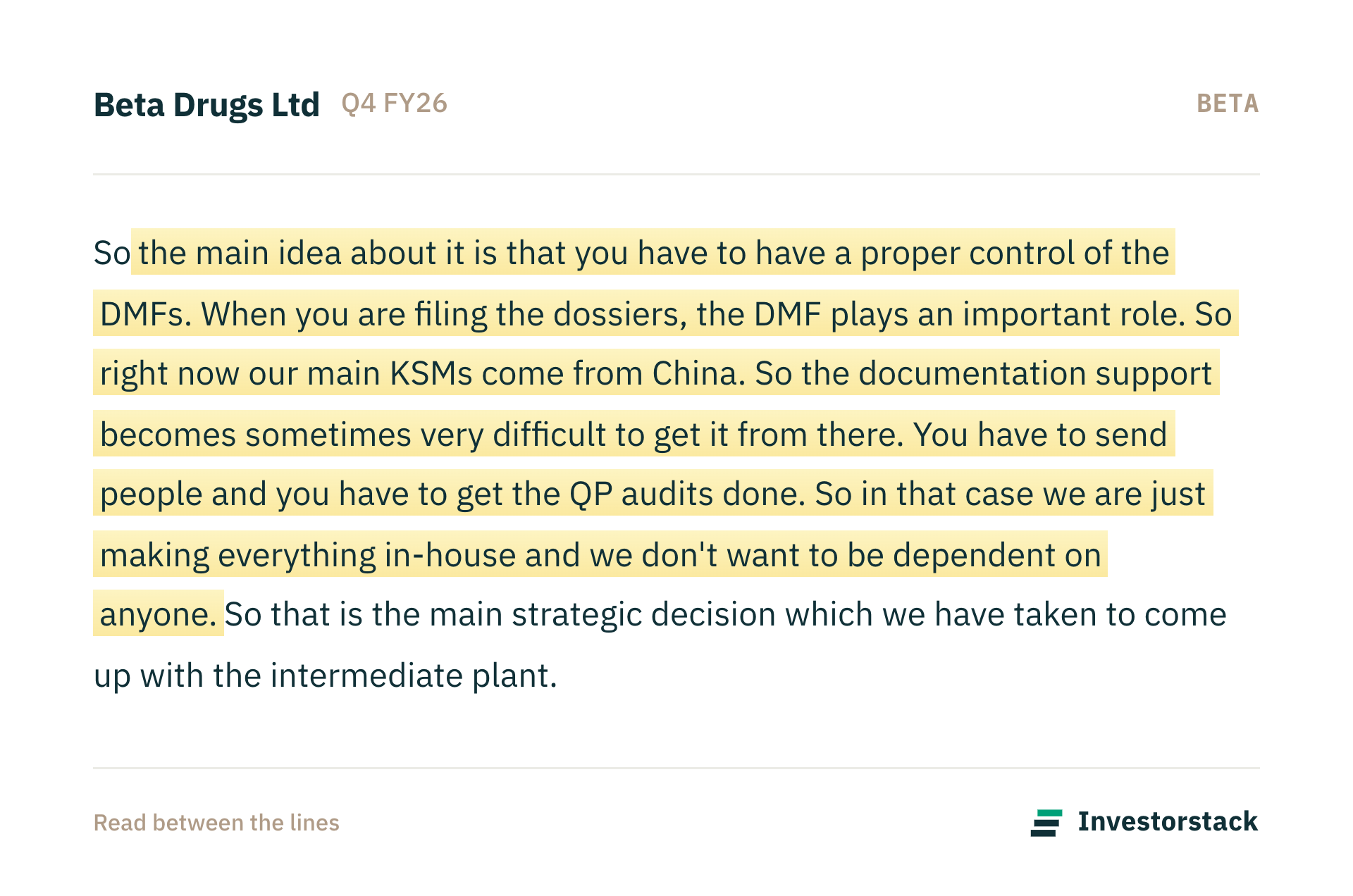

The API division contributes approximately 6% of consolidated sales as of the first half of Fiscal Year 2026 and is operated through the wholly owned subsidiary Adley Lab Limited. This segment represents the bedrock of the company’s backward integration strategy. The API plant is PIC/S-compliant and manufactures complex anti-cancer bulk drug substances. While some API production is sold directly to external domestic and international buyers, a substantial portion is consumed internally to support the formulations division. In Fiscal Year 2026, the company expanded this capability by acquiring a new intermediate chemical plant to manufacture its own key starting materials (KSMs), reducing its reliance on raw materials imported from China.

Cosmetics and Dermatology (Aesthetics)

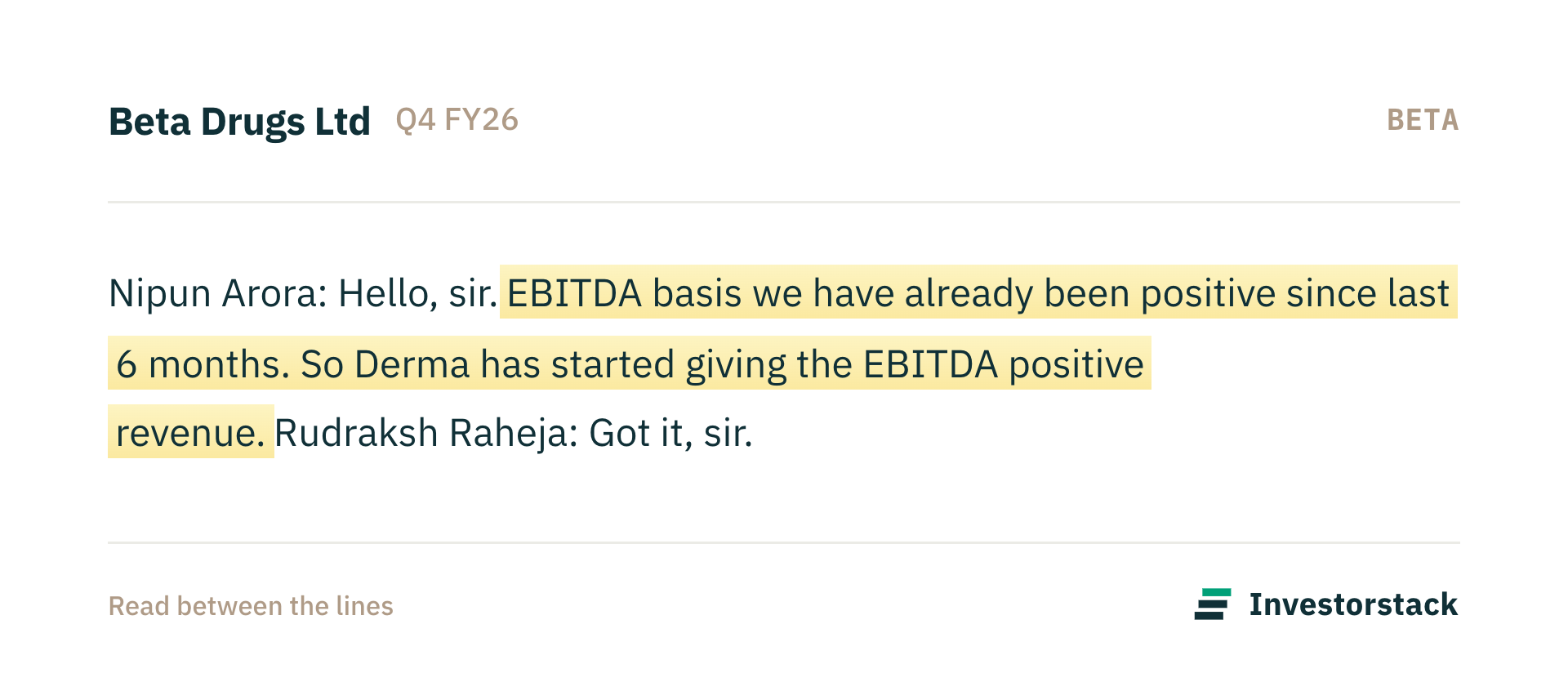

The cosmetics and dermatology division, operated under the Adley Formulations subsidiary, represents a newer, high-margin expansion area that contributes approximately 4% of total revenue. The segment focuses on medical aesthetics, dermatological therapeutics, and cosmeceuticals, and achieved EBITDA profitability for the first half of Fiscal Year 2026. The company’s strategy in this segment is driven by in-licensing unique, high-end aesthetics products, such as dermal fillers and mesotherapy products from leading European manufacturers in Italy and elsewhere, and distributing them to a growing base of dermatologists and aesthetic clinics across India.

Nivian Fertility (IVF Therapy)

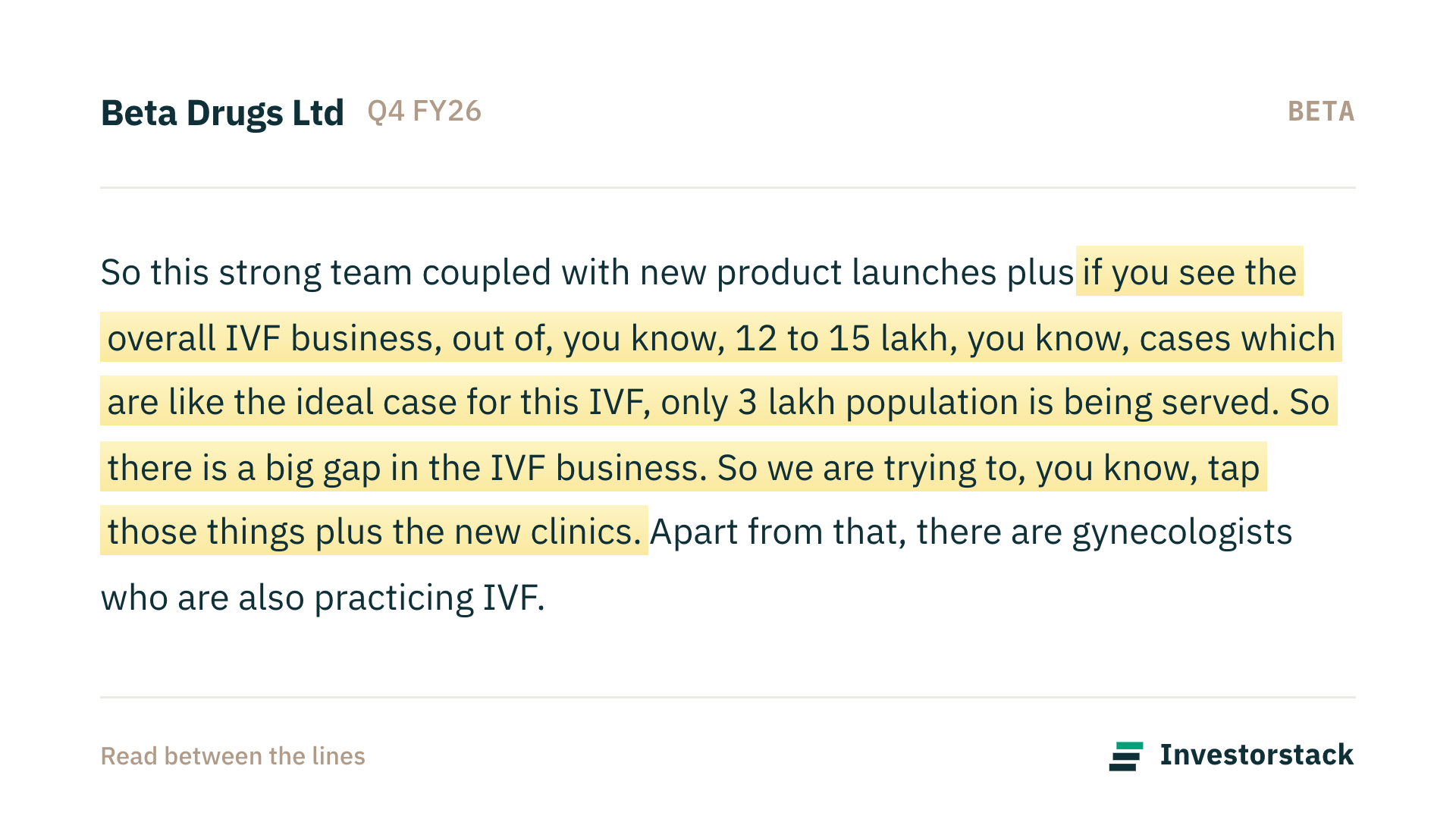

Acquired in Fiscal Year 2026, Nivian Fertility is the company’s entry into the rapidly expanding in-vitro fertilization (IVF) and reproductive health segment. Nivian operates as a branded generic division with a focus on specialized hormones and supportive therapies used in fertility treatments. The division benefits from substantial corporate hospital distribution access established by Beta Drugs over four decades. Management expects this division to grow at over 30% annually by utilizing the group’s existing institutional sales network and manufacturing infrastructure.

Products and Business Detail

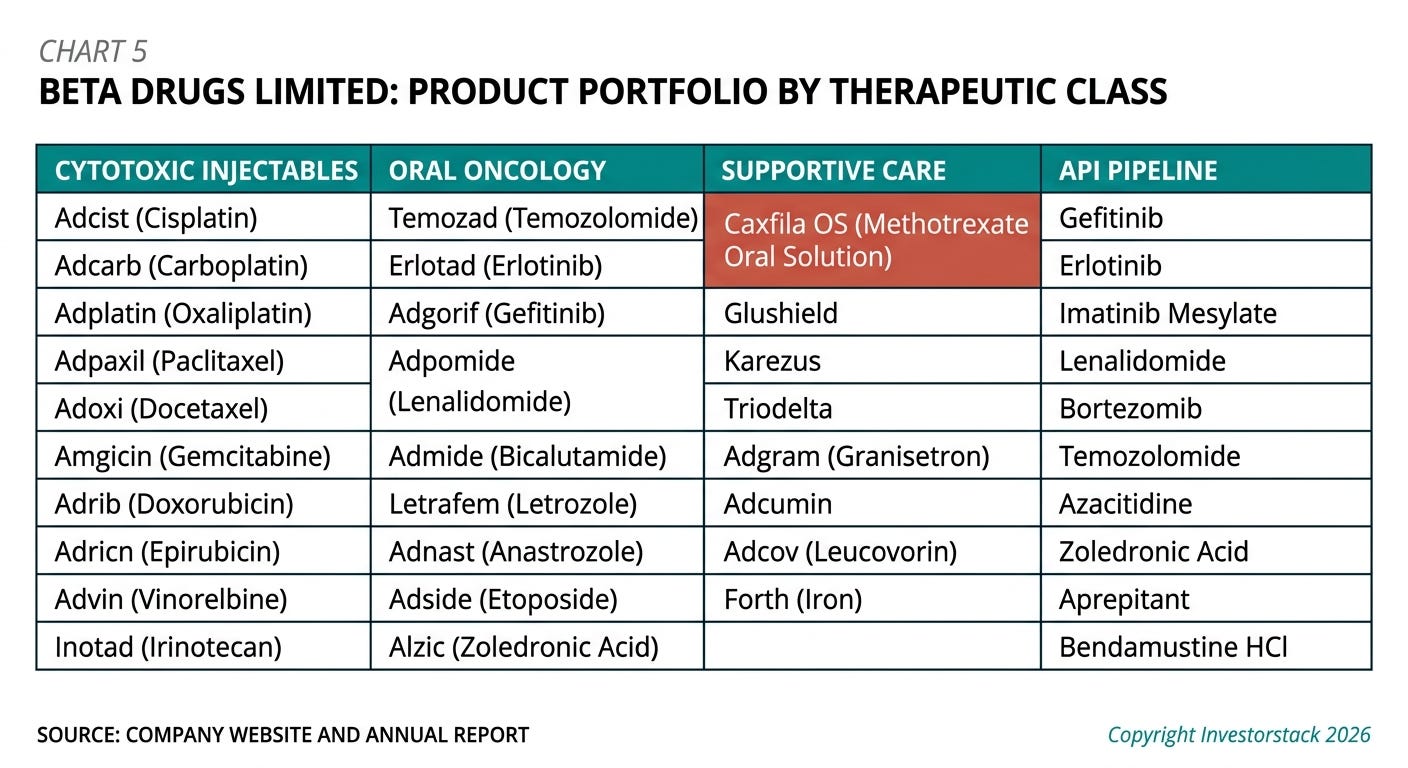

The company’s product portfolio is highly specialized, focusing entirely on oncology, aesthetics, and reproductive health. In oncology, the portfolio is divided into cytotoxic injectables, oral solid dosages (tablets and capsules), supportive care therapies, and advanced drug delivery systems. The company has a strong presence in cytotoxic oral solids, which make up 48% of its own-branded formulation sales, providing higher convenience and safety for patients compared to traditional intravenous chemotherapy.

Key oncology brands include:

Caxfila OS (Methotrexate Oral Suspension): The company’s most successful innovative product, which became the first cytotoxic suspension approved in India. Launched as a Novel Drug Delivery System (NDDS), it has reached an annual sales run rate of nearly ₹10 crore, providing a precise, easy-to-administer liquid format for pediatric and geriatric cancer patients.

Glushield: A specialized supportive care formulation used to manage side effects and toxicities associated with chemotherapy.

Adpaxil (Paclitaxel) and Adoxy (Docetaxel): Major taxane-class microtubule inhibitors used in breast, lung, and ovarian cancers.

Adcist (Cisplatin) and Adcarb (Carboplatin): Platinum-based alkylating agents used widely across solid tumors.

Temozad (Temozolomide): An oral alkylating agent used to treat brain tumors.

Letrafem (Letrozole) and Adnast (Anastrozole): Hormone-based therapies for breast cancer.

In aesthetics, under the Dermal brand, the company distributes high-end injectable fillers like SkinFill, which are in-licensed from European partners, alongside specialized mesotherapy formulations used for skin rejuvenation and anti-aging treatments. In APIs, Adley Lab manufactures bulk oncology drug substances such as Gefitinib, Erlotinib, Imatinib Mesylate, Lenalidomide, Bortezomib, and Temozolomide, alongside advanced intermediates that feed directly into the formulation pipelines.

Manufacturing is conducted across specialized, dedicated facilities:

The formulation plant in Baddi, Himachal Pradesh, handles liquid injectables, lyophilized injectables, tablets, capsules, and specialized oral suspensions under strict aseptic conditions.

The API plant in Lodhimajra, operated by Adley Lab, handles complex organic synthesis and crystallization of cytotoxic bulk drugs.

The recently acquired intermediate chemical plant provides advanced backward integration for key starting materials (KSMs), securing the supply chain against geopolitical and import disruptions.

Customers

Beta Drugs serves distinct customer profiles across its multiple business verticals:

Corporate Hospitals and Healthcare Chains: For its branded formulation division, the primary customers are large private hospital networks in India, such as Apollo Hospitals, Fortis Healthcare, Max Healthcare, and specialized oncology networks like HCG (Healthcare Global Enterprises). These customers demand high quality, reliable supply, and clinical data support.

Government Procurement and Public Health Institutions: The company is a registered supplier to major government healthcare bodies, including the Central Government Health Scheme (CGHS), Employees’ State Insurance Corporation (ESIC), railway hospitals, and military hospital networks. Procurement is typically tender-driven, focusing on cost efficiency and compliance.

Major Domestic and Multinational Pharmaceutical Companies: In its CDMO segment, the company serves as a strategic formulation supplier to top-tier Indian pharma giants, including Glenmark, Intas, Alkem, Cadila, and Torrent. These clients are highly sticky, as transferring an oncology formulation dossier to another site is a long, expensive regulatory process.

International Distributors and Health Ministries: In export markets, the company partners with local distributors and participates in national tenders run by ministries of health in Latin America, Southeast Asia, and the Middle East.

Dermatologists and Plastic Surgeons: For its aesthetics and dermatology division, the customers are private clinics, cosmetic surgeons, and specialized clinics that purchase high-margin aesthetic injectables and topical formulations.

Competitive Landscape

The structure of the Indian oncology cytotoxic market shapes how competition works. Beta operates across three competitive arenas:

Branded oncology (domestic): The Indian cytotoxic oncology market is around INR 3,000 crore in size. Beta ranks among the top 10 companies. Many of its brands hold top 5 positions in their categories. Competition comes from other Indian pharma companies with oncology portfolios, but the management emphasizes that the cytotoxic segment is narrow: few companies have the specialized manufacturing infrastructure. The NDDS products give Beta a differentiation that larger generic players cannot easily match.

CDMO (contract manufacturing): This is the most competitive segment for Beta. BDR Pharmaceuticals and Hetero Healthcare are direct competitors. SPCURA and two or three other players also compete. The CDMO business is about reliability, quality, and regulatory compliance. Beta’s advantage is that it has been doing cytotoxic manufacturing since 2005 and has built trust with the top Indian pharma MNCs. But competition is real: management expects CDMO growth of only 5-6% annually over the next few years.

Exports: In unregulated and semi-regulated markets, competition comes from other Indian generic manufacturers. But Beta’s strategy is to file dossiers early and be among the first 2-3 generics to enter a market. With over 200 dossiers filed in the last 1.5 years and ~100 expected new registrations in FY27, the company is building a first-mover advantage in many countries. Once the EU GMP audit is cleared (scheduled for September 2026), Beta will be able to export to regulated markets where competition is less intense and margins are higher.

What wins and what loses: Beta wins on three factors: (1) the specialized nature of cytotoxic manufacturing, which limits the number of qualified players; (2) the NDDS formulations that are difficult to replicate; (3) the long-standing relationships with CDMO partners. It loses when it gets stuck in commoditized products like Platins, where NPPA pricing crushes margins. It also faces the risk that larger CDMO players might build capacity and compete aggressively on price.

The Nivian acquisition: In IVF, competition is fragmented. Nivian has a 4.5% market share. The recombinant segment (INR 1,000 crore of the INR 2,000 crore market) is dominated by large biotech companies. Beta plans to in-license recombinants to expand into that segment.

Beta Drugs establishes its competitive edge through several distinct advantages:

Deep Backward Integration: Unlike many competitors who import active ingredients and intermediate chemicals from China, Beta Drugs manufactures its APIs and intermediates in-house. This complete control over the chemical synthesis chain allows it to maintain consistent margins and supply continuity, especially during global disruptions.

Focus on Novel Drug Delivery Systems (NDDS): The company actively avoids the highly commoditized generic space by focusing on differentiated formulations like Caxfila OS (the first cytotoxic suspension approved in India) and upcoming oral liquid pipelines. This R&D focus shields it from severe price erosion.

Highly Sticky CDMO Relationships: Because regulatory guidelines mandate that a change in contract manufacturing site requires extensive bioequivalence testing and dossier refiling, the switching costs for its CDMO clients (like Glenmark and Intas) are exceptionally high. The company has not lost a single CDMO partner in the last five years.

Low-Cost Manufacturing Base: The company’s consolidated manufacturing operations in Himachal Pradesh offer significant cost efficiencies, allowing it to compete aggressively in global tender markets while maintaining high operating margins.

Industry

The oncology market is one of the fastest-growing therapeutic segments globally, driven by rising cancer incidence, improved diagnostics, and increasing access to specialized healthcare in emerging economies. In India, the cytotoxic oncology formulation market is valued at approximately ₹3,000 crore and is projected to expand to over ₹4,000 crore by 2028, growing at a compound annual rate of over 10%.

Key structural dynamics shaping the industry include:

Regulatory Approvals and Compliance: The global pharmaceutical industry is heavily regulated. Companies must obtain approvals from local health authorities, such as COFEPRIS in Mexico, INVIMA in Colombia, and the European Medicines Agency (EMA) for Europe, to export formulations. These audits require multimillion-dollar facility upgrades and rigorous clinical documentation.

Transition to Oral Therapies: There is a significant structural shift from hospital-administered intravenous chemotherapy to self-administered oral oncology therapies (tablets, capsules, and oral liquids). This shift improves patient compliance, reduces hospital stays, and offers higher-margin opportunities for manufacturers. Oral formulations now represent 48% of Beta Drugs’ own branded formulation sales.

Import Substitution and Active Ingredient Security: Historically, Indian formulation manufacturers have been heavily dependent on active ingredients and starting materials imported from China. Due to supply chain vulnerabilities exposed during recent years, there is a strong industry push toward local manufacturing of starting materials. The company’s expansion into its own intermediate facility directly addresses this critical structural trend.

Expansion of Medical Aesthetics: The medical aesthetics and anti-aging market in India is growing at over 14% annually, driven by rising disposable incomes, urban modernization, and a growing acceptance of non-invasive cosmetic procedures. This non-regulatory, cash-pay market offers rapid cash conversion and high margins, providing an excellent counter-cyclical hedge to the institutional oncology business.

Growth Triggers

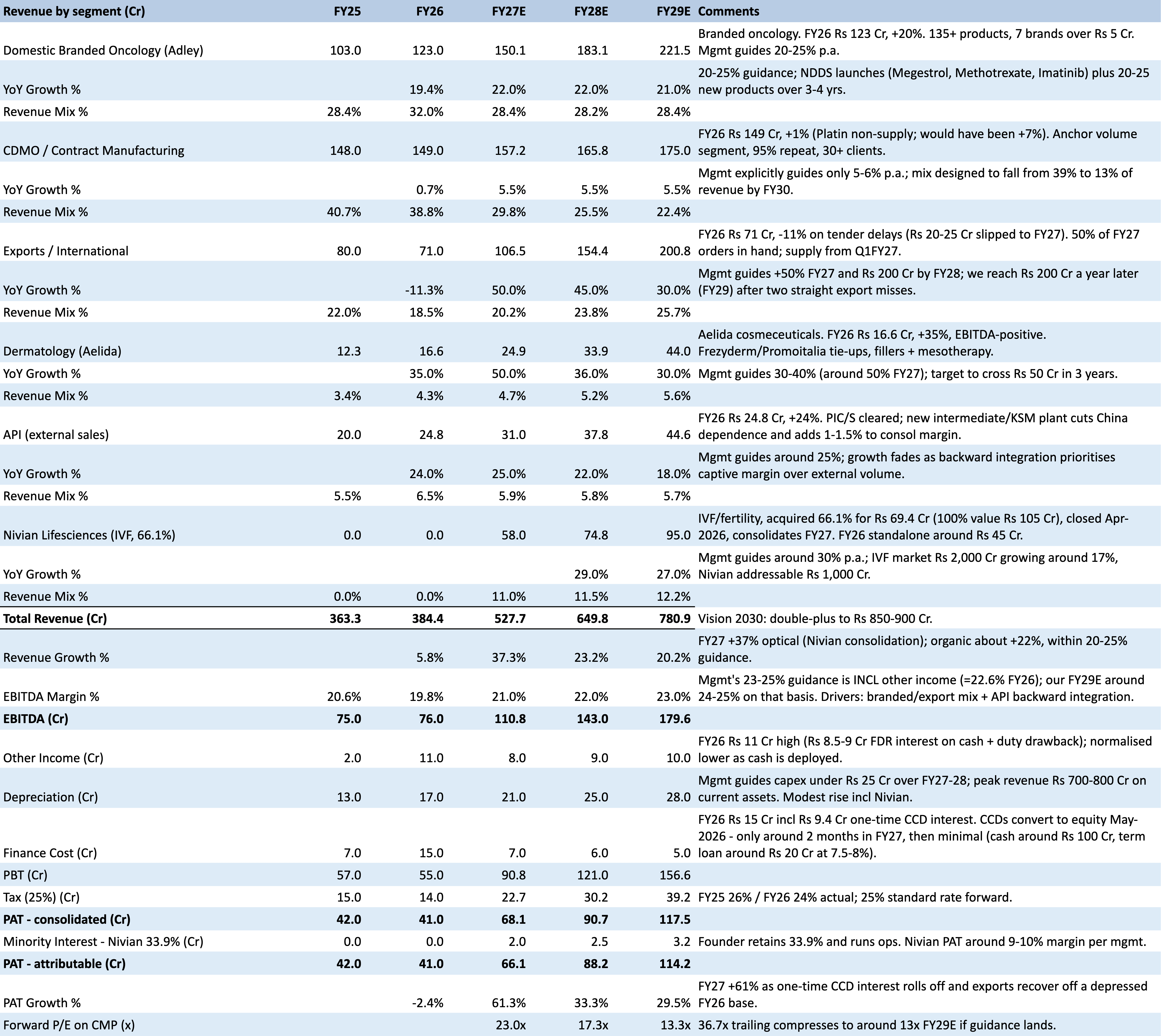

Delayed export tenders now awarded, worth INR 20-25 crore, will start supplying from Q1 FY27. This reverses the 11% export decline in FY26. Management expects 50%+ export growth in FY27.

Nivian Lifesciences acquisition (66.1% stake, closed April 2026) adds a fertility/IVF vertical. Nivian had INR 45-46 crore revenue and 18-19% EBITDA margins in FY26. Management expects 30% annual growth from this segment. Full consolidation begins FY27.

Two new NDDS products to launch in FY27. One (Imatinib solution) in the next 2 months, another by January-February 2027. These are first-in-India oral solutions that have historically expanded markets (Megestrol acetate went from INR 6 crore to INR 16 crore market).

Backward integration – intermediate plant to reduce China dependency. The company spent ~INR 27 crore on a plant to manufacture KSMs in-house. Commercialization expected by end of FY27. Management estimates 1-1.5% margin improvement, plus better DMF control for regulated market filings.

Derma/cosmetology division scaling toward INR 50 crore in 3 years. The division grew 35% to INR 16.58 crore in FY26 and turned EBITDA positive. Management targets 30-40% annual growth with EBITDA margins improving to 12-14% at scale. Exclusive European filler and mesotherapy approvals add niche.

More than 200 dossiers submitted; expecting ~100 new registrations in FY27. These span 14 new countries. The company plans to operate in 45 countries and expects top 5 countries to contribute 30% of export sales.

Key Risks

Concentration in government tender exports creates lumpy, unpredictable revenue. 90% of oncology business globally is tender-based. Public sector delays pushed INR 20-25 crore of orders from FY26 to FY27. This is structural, not fixable – Beta cannot control when governments issue or award tenders. A single-country delay can swing quarterly results significantly.

NPPA price control on Platins squeezes domestic margins. The cost of Carboplatin (~INR 2,300-2,400 per vial) is close to the NPPA fixed price (INR 2,850), leaving no room after distributor discounts. Beta essentially stopped domestic Platin supply in H2 FY26. Since Platins are the basic chemotherapy protocol, this creates a gap in the product basket that must be filled with other molecules.

Raw material price and foreign exchange volatility. Key inputs are byproducts of petrol; Beta stockpiles 5 months of supply as a buffer. While the company can pass on increases in export and CDMO contracts, the branded domestic business absorbs pressure. Any sustained spike could compress gross margins.

Regulatory delays in market entry timelines. EU audit was expected between January-March 2026 (stated in Nov 2025) but got pushed to September 2026 due to a new rule requiring dossiers to be filed first. Each country registration takes 18-36 months. The gap between dossier filing and revenue realization is long, and setbacks compound.

Competition in CDMO and branded oncology. Companies like BDR Pharmaceuticals, Hetero, and SPCURA compete directly for CDMO contracts. In branded oncology, Beta is among the top 10 but faces larger MNCs with deeper R&D budgets. Differentiation relies on quality and innovation (NDDS), but pricing pressure is constant.

Integration risk from Nivian acquisition. Though the promoter stayed on, Beta must realize procurement synergies, cross-sell into corporate hospitals, and maintain growth momentum. Any execution misstep in combining teams, systems, or customer relationships could dilute the 30% growth assumption.

Walk the Talk

4/5. Management Delivered on Key Promises in API, Exports, and EU Audit

Beta Drugs fulfilled critical promises on API backward integration, export dossier filings, and EU audit completion. Export revenue grew 73% YoY, and the Eurasia audit was successfully concluded. However, the derma segment remains unprofitable despite earlier guidance of breakeven by FY25.

Scenarios & Valuation

Bull case

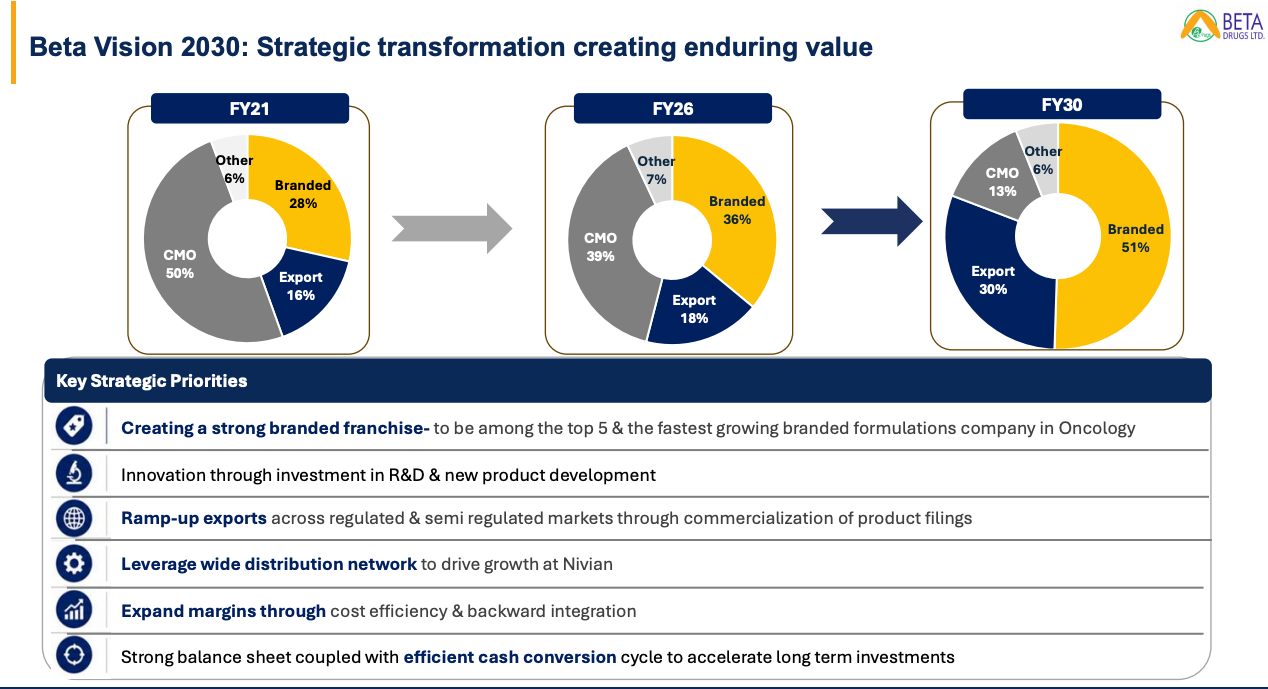

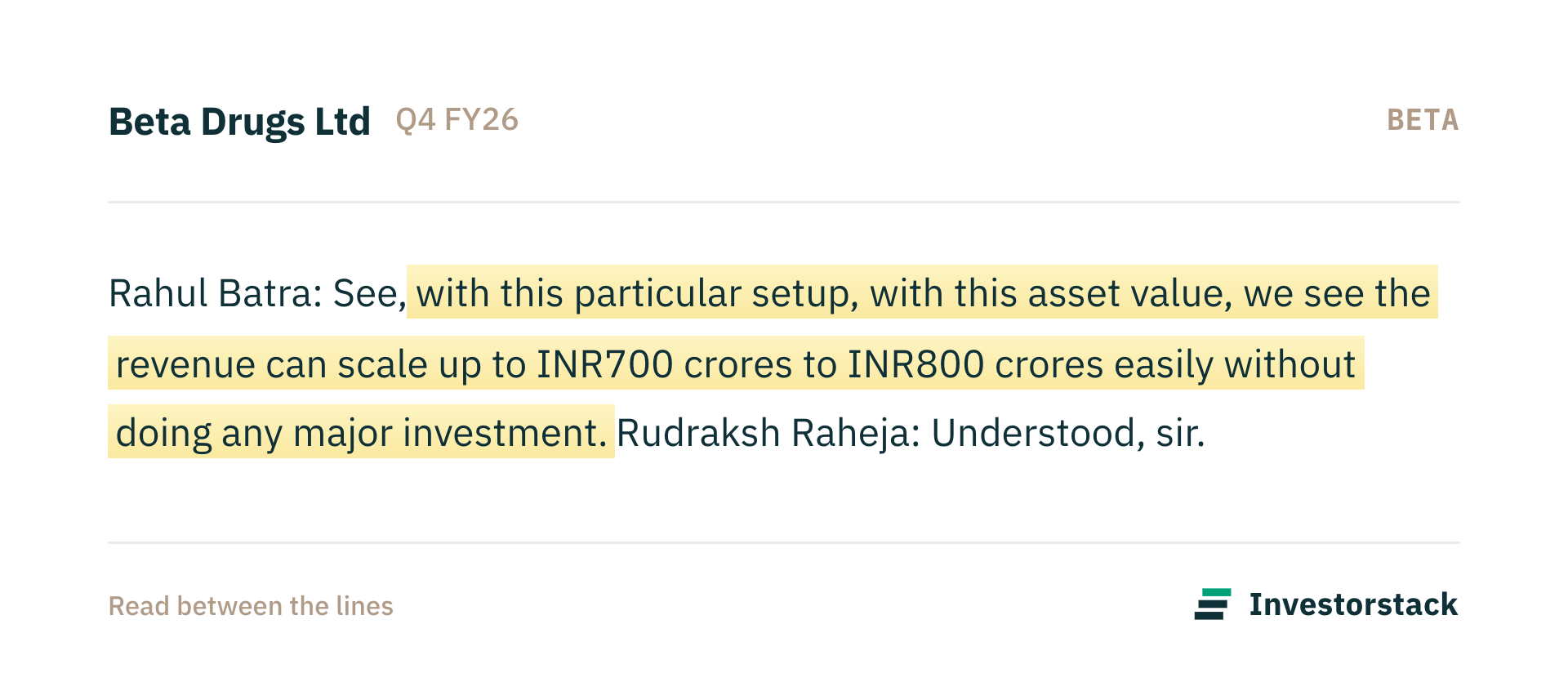

The export tenders awarded in March 2026 flow smoothly through FY27, generating the 50% growth management expects. EU GMP audit in September 2026 passes without critical observations, and within 2.5 years Beta enters regulated markets with first-to-file dossiers on niche molecules. The intermediate plant reaches commercial production by end of FY27, reducing China dependency and improving margins by 1-1.5% as forecast. Nivian integration exceeds expectations: the promoter team maintains 30% organic growth while Beta’s hospital access doubles IVF product offtake. The two new NDDS launches gain quick prescription share. Derma crosses INR 30 crore in FY28 with 12% EBITDA margins. By FY30, the company achieves its INR 900 crore vision with exports at 30% of revenue and branded oncology at 51%, transforming from a domestic CDMO player to a diversified specialty pharma with global regulated market presence.

Base case

Export growth recovers to 30-40% in FY27 as delayed tenders are fulfilled, but some new tender delays recur, keeping the segment lumpy. EU audit happens in September 2026 but the certificate takes 9 months; meaningful regulated market revenue begins only in FY29-30. The intermediate plant commercializes but initial yields are lower than expected; margin improvement is 0.5-1% rather than the aspirational 1.5%. Branded oncology grows at 20-22% annually, driven by NDDS launches but offset by continued domestic Platin supply constraints. Nivian grows at 20-25%, slightly below the 30% target, as integration takes time. The company reaches INR 700-750 crore by FY30, missing the aspirational INR 900 crore but maintaining 22-24% EBITDA margins. Management continues to set ambitious targets and often delay them, but the core business of oncology formulations remains steady and profitable.

Bear case

Export tender delays recur in FY27, limiting growth to 15-20% instead of 50%. One of the two NDDS launches gets held up at CDSCO or NPPA pricing, delaying the branded growth engine. The EU audit reveals quality observations requiring re-inspection; the timeline slips to FY28-29. The intermediate plant encounters technical problems in scale-up, with CAPEX exceeding the INR 27 crore estimate and commercial production pushed to FY28 or beyond. Platin pricing remains unviable in domestic markets, forcing continued supply constraints. Nivian’s growth disappoints as the IVF market sees increased competition from larger players and the 4.5% market share proves hard to defend. Gross margins compress as CDMO partners demand price reductions and export tenders get increasingly competitive. The FY27 revenue target is missed by 10-15%, and the Vision 2030 of INR 900 crore is publicly walked back. Questions about management’s execution credibility grow louder with each delayed regulatory milestone and missed revenue forecast.

Thanks for reading! Do check out Investorstack.