Inox India: Play on Semiconductor and Datacenter Boom

How a 1976 backward-integration play became India's only credible cryogenic equipment maker, and why the next five years could rerate it.

Before we begin, Check our Investorstack - Your one stop destination to become

a better investor.

Here’s what you get:

Research Reports for more than 1000 companies!

Sector Intelligence Briefs

Industry Dashboards: Live RS ratings, dominant market stages, and sentiment across every industry.

Growth triggers, management consistency checks, walk the talk, thesis maps

and much more. Check out the landing page for an interactive demo.

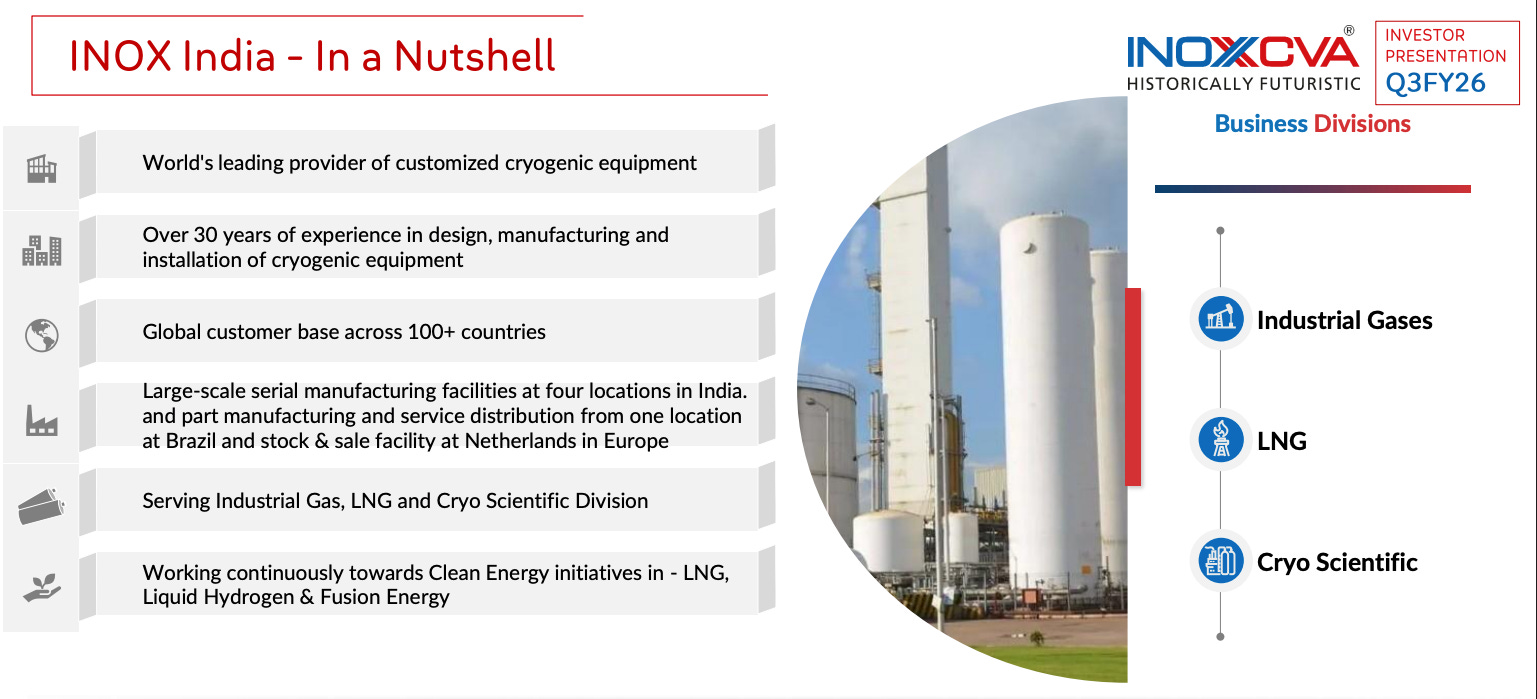

Inox india is a vadodara based manufacturer of cryogenic equipment - tanks, systems, and turnkey installations that keep gases in their liquid form at temperatures ranging from -73°C all the way down to -271°C. If you have ever wondered how a steel plant gets its liquid oxygen, or how a hospital in rural india stores liquid nitrogen, or how an ISRO rocket fuels up with liquid hydrogen - the answer, in india and increasingly across the world, often involves a tank built by inox india.

The company was incorporated in 1976 as baroda oxygen limited, a subsidiary of the inox group - the same gujarati conglomerate that owns inox air products, inox wind, and (until recently) pvr inox cinemas. The original impulse was backward integration: the inox group was importing cryogenic tanks from the us, europe, and japan, and the lead times stretched beyond a year. Rather than depend on foreign suppliers for equipment that was foundational to their own industrial gas business, the promoters decided to build it themselves. That factory in vadodara opened in 1992, and the current company is the result of three decades of accumulated engineering experience in a field where the learning curve is steep and certifications are demanding.

The pivotal strategic move came in 2009, when inox india acquired a majority stake in cryogenic vessel alternatives (cva), a us-based manufacturer with a european presence. The combined entity operates under the brand inoxcva and now has manufacturing and service operations in india (vadodara and kalol, gujarat; silvassa), brazil (indaiatuba, são paulo), and europe (alblasserdam, netherlands). The brazil unit opened in 2016, specifically to serve south american customers with locally produced products and repair services.

What inox india actually makes is equipment for storing, transporting, and distributing cryogenic liquids - gases that have been cooled below their boiling points until they liquefy. Liquefying a gas compresses it to roughly 1/600th of its gaseous volume, which makes large-scale storage and long-distance transport economically viable. the core technology is vacuum insulation: a double-walled stainless steel vessel with a vacuum jacket between the walls, sometimes supplemented with perlite insulation, that slows heat ingress enough to keep the contents liquid for extended periods. Building this reliably - especially for large tanks, dangerous gases, and extreme applications like space propulsion or nuclear fusion - requires metallurgical expertise, precision fabrication, certified welding, and strict quality management.

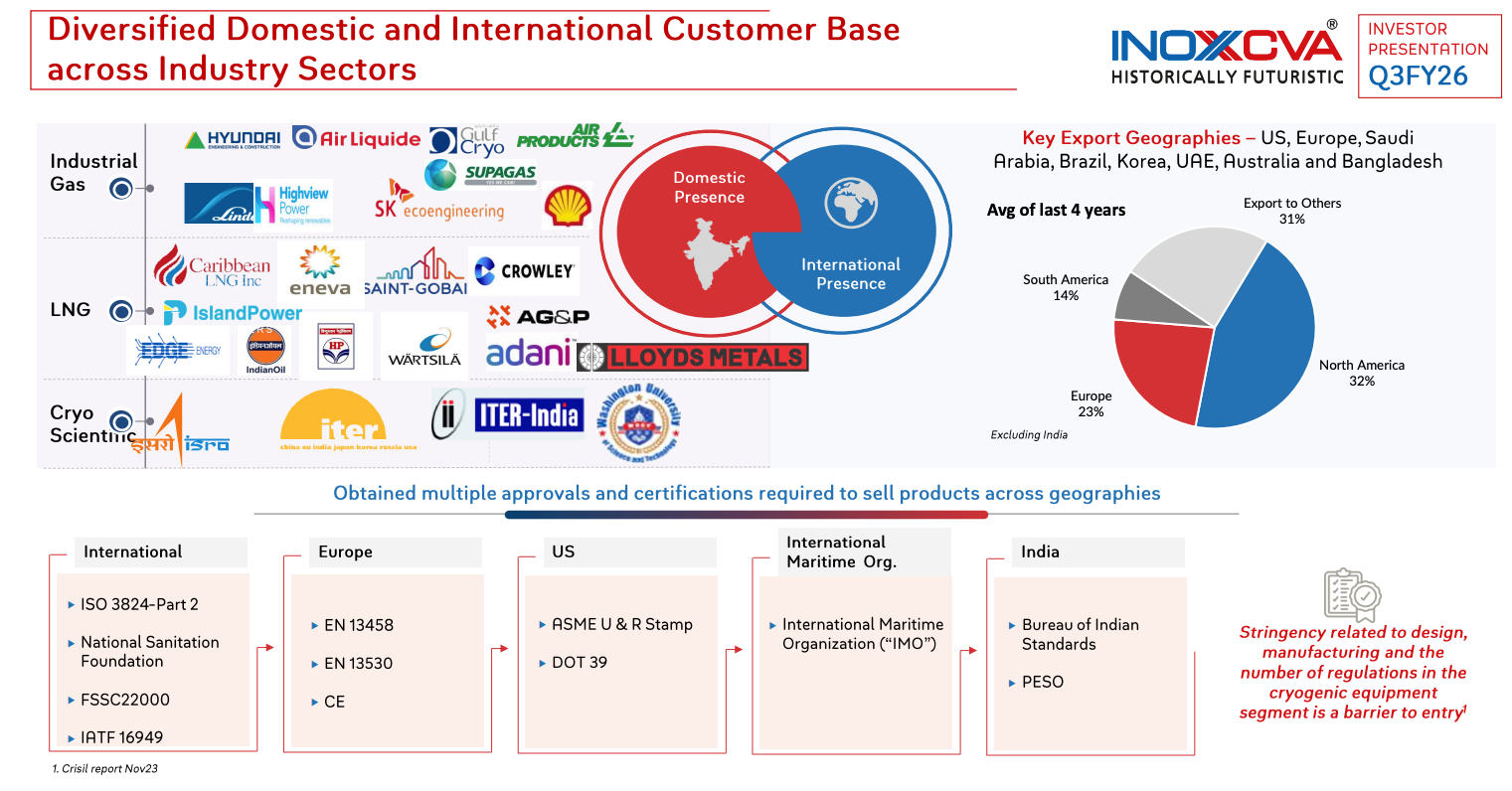

The company serves customers across more than 100 countries, with after-sales support associates in 25 countries. as of the most recent data, it employs approximately 1,230 people. promoter holding stands at 75%, steady and unchanged.

Business Segments

Inox india operates across four business divisions. Three are disclosed as segments: industrial gas solutions, lng, and cryo scientific division (csd). beverage kegs / sustainable industrial packaging sits as a fourth product category within the same manufacturing infrastructure.

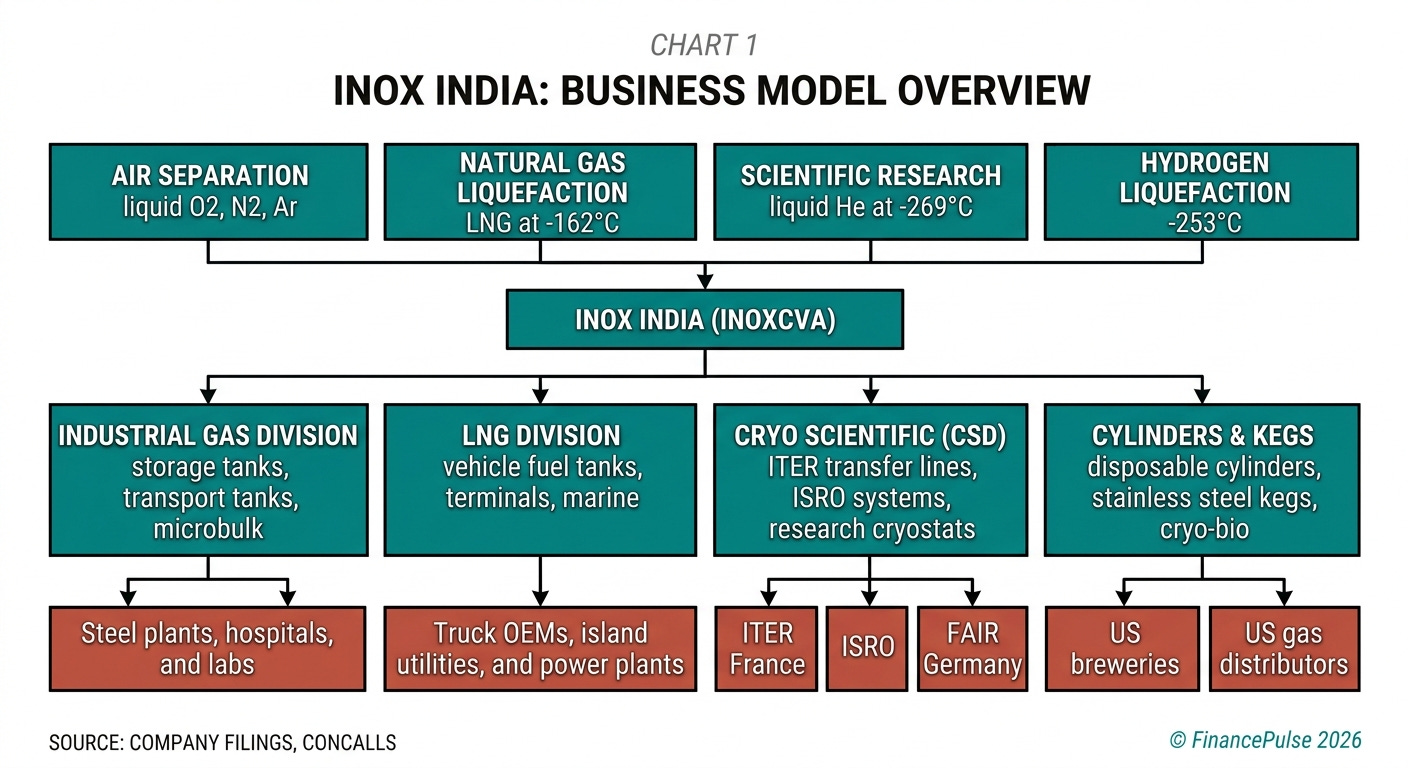

Industrial gas solutions

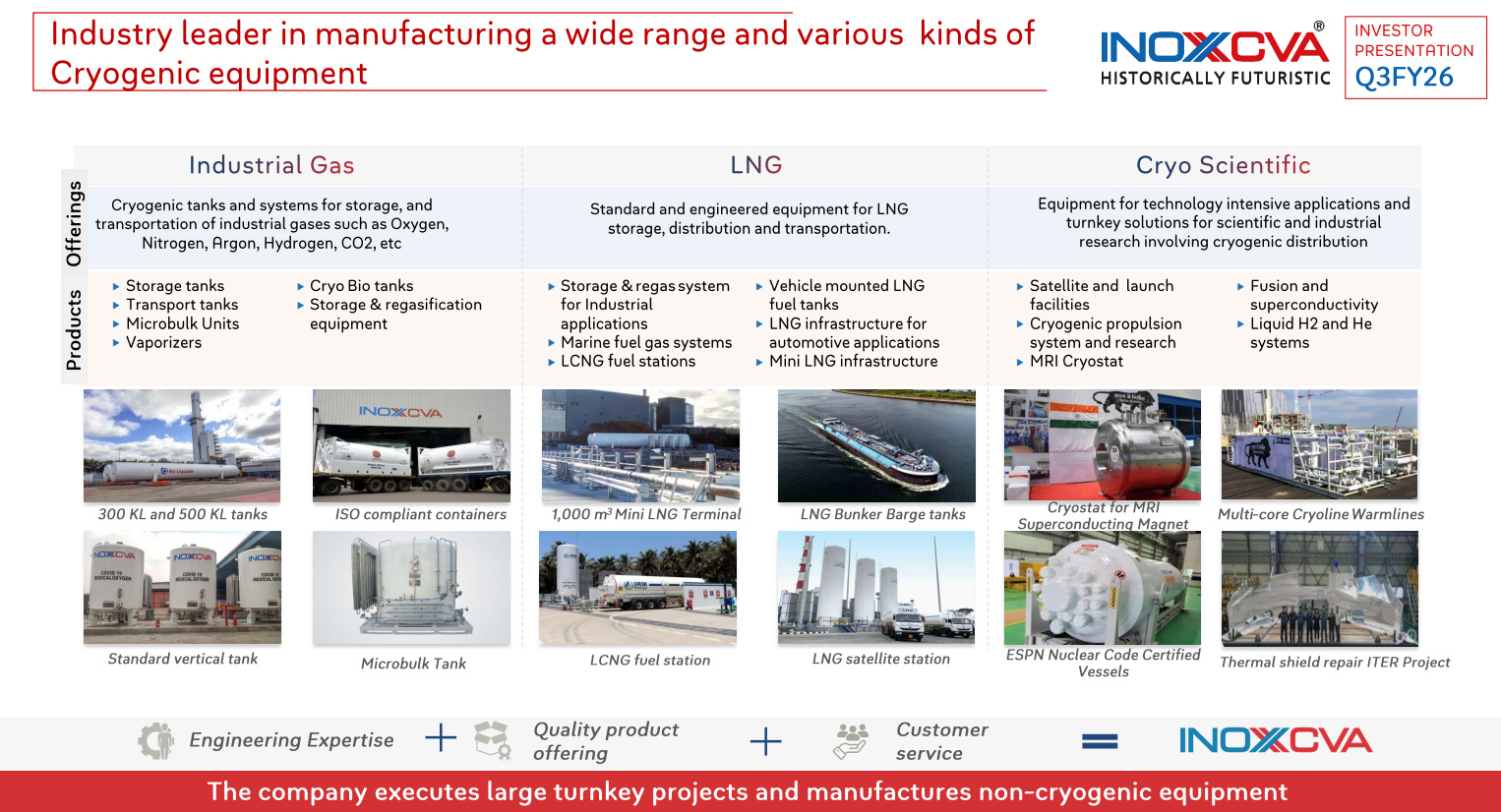

This is the backbone of the business. For the full year fy25, this segment contributed approximately 65% of revenue and 56% of order inflows. It makes, installs, and services cryogenic tanks and systems used to store and distribute industrial gases - liquid oxygen, liquid nitrogen, liquid argon, carbon dioxide, ethylene oxide, and increasingly, green hydrogen.

The core product here is the storage tank - a vertical or horizontal double-walled vacuum-insulated vessel ranging from small “microbulk” units of a few hundred liters (used by hospitals, labs, and small manufacturers) up to large flat-bottom tanks holding tens of thousands of cubic meters (used by steel plants and gas terminals). The company also makes transport tanks (iso containers and tankers) and vaporizers that convert liquid back to gas for end-use.

The customers are primarily the large industrial gas companies - air liquide, linde, air products, messer, taiyo nippon sanso, gulf cryo. These companies own and operate the air separation units that produce oxygen and nitrogen, then use inox india’s tanks to store and deliver the gases to end customers. this creates a specific commercial dynamic: inox india is a supplier to the gas companies, not to the end-use industries directly. The gas companies care intensely about reliability and certifications, because a tank failure in a hospital oxygen supply or a steel plant has severe consequences. they are not buying on price alone.

Inox india’s newest growth product within this segment is ultra-high purity ammonia iso containers for the semiconductor and solar industries - a product the company described in its q1 fy26 concall as india’s first of its kind, targeting the expanding semiconductor fabs being built across india and globally. The company also recently introduced co2 battery storage solutions, securing a pilot order from italy in q1 fy26, with management describing “global potential.” The segment is also supplying liquid helium containers and specialized tanks for semiconductor applications in the us - nine such tanks were delivered to a us semiconductor customer in q4 fy25.

LNG division

the LNG division designs, manufactures, and installs equipment for liquefied natural gas storage, distribution, transportation, and infrastructure. LNG sits at -162°C, requiring specialized insulation and safety engineering beyond standard industrial gas equipment.

there are three distinct sub-markets within this division:

LNG vehicle fuel tanks. Inox india supplies cryogenic fuel tanks to heavy-duty truck oems - tata motors, ashok leyland, and others. The tanks are mounted on lng-powered trucks and buses. In q1 fy26, the company supplied approximately 145 such fuel tanks in a single quarter. The kalol facility (in panchmahal, gujarat) is dedicated to this product and is being expanded - management described in the q2 fy26 concall plans to “scale our lng drill tank production up by 10x over the next few years.” In february 2025, inox india became india’s first cryogenic equipment manufacturer to receive the iatf 16949 certification from bureau veritas for this product category, which is a mandatory requirement for direct supply to automotive oems. This certification removes a previously real barrier to entry into the oem supply chain.

Management has consistently described lng as a “winner fuel” for heavy trucks over the next 8-10 years. The argument: lng cuts co2 by 20-30% versus diesel, extends range, and costs less per kilometer. The regulatory environment is shifting - the small and medium pressure vessel (smpv) rules were amended to approve lng as a vehicle fuel, which unlocked broader adoption. The company holds over 85% market share in lng semitrailers operating on indian roads.

LNG infrastructure. Inox india builds small-scale lng terminals - satellite stations, dispensing stations, and mini-terminals for islands and remote industrial users who cannot access the main gas pipeline network. It commissioned 6 lng dispensing stations in fy24, completed the antigua mini-lng terminal (4 x 1,000 m3 tanks), and in november 2024, won a major order from island power producer ltd. In the bahamas for 10 x 1,500 m3 lng storage tanks and a regasification system for a power plant. This was followed in q2 fy26 by two additional satellite lng power station projects from small island nations near the bahamas.

In fy25, the company commissioned a 33 m3 LNG semi-trailer in Taiwan. In q3 fy26, it secured orders for LNG storage tanks for an LNG terminal project in Africa (2 tanks of 500 m3 each) and LNG marine fuel tanks from a European customer for two tanks of 150 m3 each.

LNG regasification and station infrastructure within india. The government has long-term ambitions to build 1,000+ LNG dispensing stations along indian highways for truck fueling. Actual rollout has been slower than targeted. As of q2 fy26, only around 50 stations were operational or imminent. management acknowledged on the q2 fy26 concall: “LNG station somehow is not picking up that fast to our expectation. but definitely, some private [players are coming].” this slower-than-expected pace is the single most visible execution gap in the LNG story.

Cryo scientific division (CSD)

This is the highest-margin, most technically complex, and most prestigious segment. it works on large bespoke projects for global scientific and research institutions. The products are not commercial catalog items - they are one-of-a-kind systems engineered for specific experiments involving temperatures near absolute zero.

The most prominent project is ITER, the international thermonuclear experimental reactor being built in cadarache, france. ITER is a multinational fusion energy project - effectively a machine designed to demonstrate that nuclear fusion can produce more energy than it consumes. It requires some of the most demanding cryogenic engineering in existence: superconducting magnets that must be cooled to near absolute zero using liquid helium, and inox india has been manufacturing multi-process vacuum-jacketed transfer lines for the iter site. In q2 fy26, the company received two major refurbishment contracts for ITER - a vacuum vessel thermal shield repair for sector f and a cryostat thermal shield repair. The q2 fy26 transcript stated: “these projects underscore our ongoing partnership with global scientific research institutions and reaffirm our execution excellence at a complex cryogenic facility.”

The division is also bidding for projects at fair (the facility for antiproton and ion research in germany), and has been working closely with ISRO on cryogenic systems for the indian space program. The company was the first indian manufacturer to build a trailer-mounted hydrogen transport tank, designed jointly with isro. On the q1 fy26 concall, management mentioned a large isro tender (described as worth approximately rs 4,000 crore) and noted they were working closely with isro and expected an rfq by december 2025.

The csd contributed approximately 23% of q1 fy26 revenue. it is lumpy by nature - revenue depends on milestone billings from multi-year projects. order inflows can be volatile because single orders are large (the iter cryostat thermal shield order alone was rs 145 crore per q1 fy26 concall data).

Beverage kegs and sustainable industrial packaging

Inox india leverages its stainless steel fabrication and container expertise to manufacture stainless steel beverage kegs for the global brewing industry. The company had approvals from certain breweries and was awaiting approvals from heineken and ab inbev as of q2 fy26. Management confirmed on the q3 fy26 concall that both approvals had been secured, and that the company held approximately 40% exposure in that market segment.

The keg business is seasonal - peak demand runs january through july, aligned with summer brewing cycles in europe and north america. It is a lower-complexity product than cryogenic vessels but uses the same manufacturing infrastructure, providing incremental utilization.

The company also makes cryobio containers (liquid nitrogen containers for livestock semen preservation and pharmaceutical biosamples), disposable refrigerant cylinders, and helium balloon cylinders. The disposable cylinder segment has been growing - management guided for 2 to 2.5 million cylinders annually in the q2 fy26 concall, with approximately 500,000 manufactured in h1 fy26. A us customer placed an order for over 700,000 disposable cylinders in q3 fy26 alone.

Customers

The customer base divides neatly into three tiers by end market.

Large industrial gas companies are the dominant buyer segment for the industrial gas division. air liquide, linde, air products, messer, taiyo nippon sanso, gulf cryo, and praxair (now part of linde) collectively account for a large share of the order book. These companies need cryogenic tanks as fundamental infrastructure for their gas distribution businesses. They are repeat buyers - every time they expand storage capacity or build a new distribution terminal anywhere in the world, they need to procure tanks. The switching costs are high: the gas companies have approved supplier lists, and getting on to the list requires certifications, audits, reference installations, and track record. Once you are approved, the gas company defaults to you for repeat orders unless something goes wrong.

The dynamic is somewhat unusual: inox india’s customers (the gas companies) are simultaneously competitors to inox india’s promoter group (inox air products, which is itself an industrial gas manufacturer). This potential conflict is managed through the listed entity’s independent operations and has not been publicly identified as a material issue.

isro, iter, research institutions are the cryo scientific customers. iter is a multi-year, multi-crore relationship. isro relationships go back to the hydrogen transport tank collaboration. the fair project in germany would be a new marquee client. these customers don’t buy standard products - they buy engineering capability, manufacturing precision, and the ability to deliver to specs that no one else in india (and few globally) can meet. the switching cost here is extremely high - replacing a supplier mid-project for a nuclear fusion reactor is not something that happens.

Oems and infrastructure developers are the LNG customers. tata motors and ashok leyland buy fuel tanks for lng truck programs. island governments and private power producers commission mini-lng terminals. shell, total, and downstream distributors buy lng storage. the bahamas contract with island power producer ltd is a good example: a power utility on an island without gas pipeline connectivity needs to import lng by ship, store it, regasify it, and burn it for electricity. the entire system - storage, regasification, distribution - is a turnkey order.

Competitive Landscape

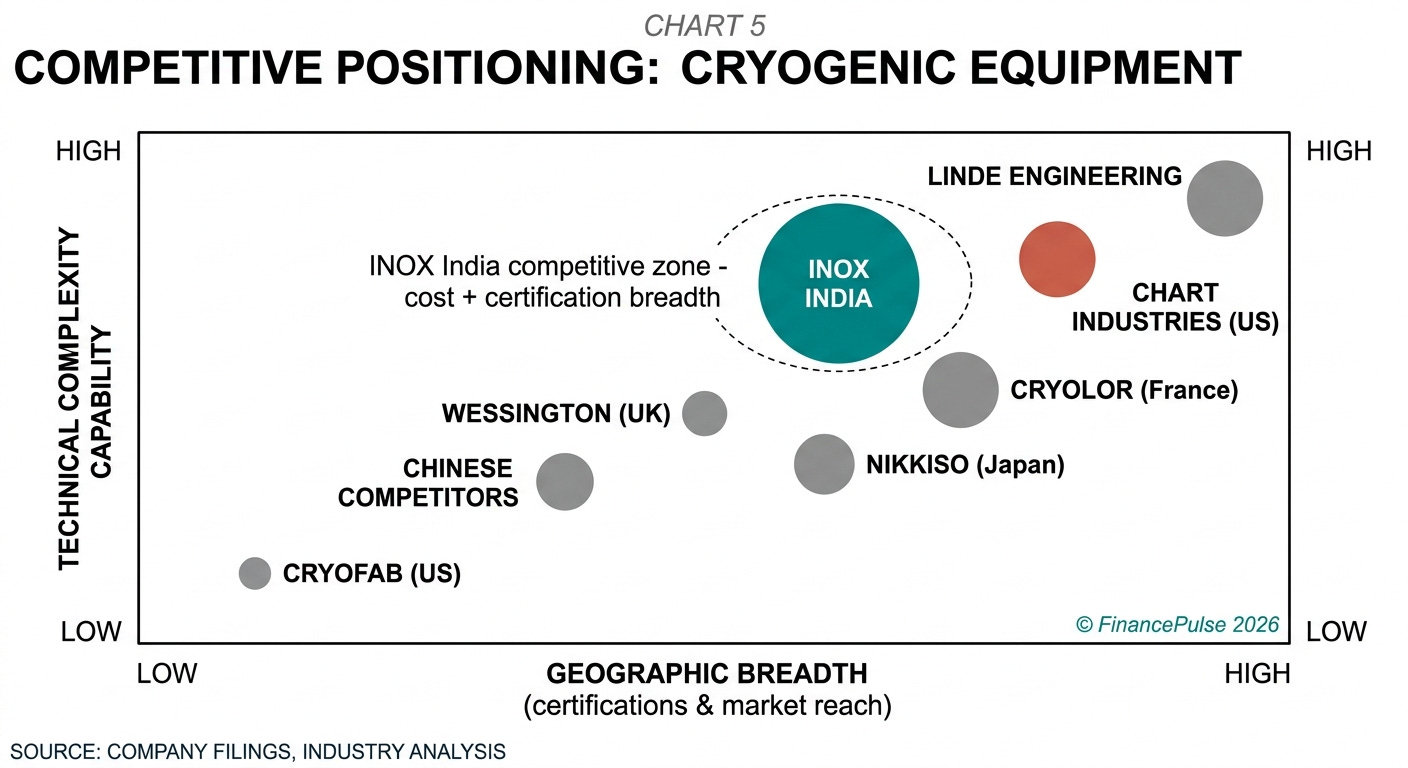

The global picture. The global cryogenic equipment market peers include chart industries (us), linde (germany/us), nikkiso (japan), wessington cryogenics (uk), cryolor (france, now a chart subsidiary), cryofab (us), isisan (turkey), lapesa (spain), and vrv spa (italy). Chart industries is the scale comparison: it is a much larger, publicly traded us company with multiple acquisitions and a broader product portfolio. linde is vertically integrated - it makes the gases and the equipment.

Where inox india fits. Inox india is not competing with chart for the very large lng import terminals or complex us natural gas infrastructure. It competes on standard and mid-complexity industrial gas tanks globally, on lng infrastructure for small-scale and island markets, and on cryo scientific projects where its iter relationship and isro collaboration create credibility.

Why inox india wins orders in industrial gas. Cost is the primary factor. Inox india’s manufacturing cost base in india - even accounting for freight - is substantially lower than a european or us manufacturer. an industrial gas tank that would cost x from linde engineering or chart will cost materially less from inox india, with comparable quality (evidenced by the fact that air liquide, linde as gas distribution customers, and others consistently reorder). Once a customer has taken delivery of tanks from inox india and verified quality through installation and operation, subsequent purchases become easier. The customer has already done the audit, approved the factory, and trained maintenance staff on the equipment design.

The second factor is certification breadth. inox india carries approvals for virtually every major market - asme for the us, ce for europe, as1210 for australia, kgsc for korea, gb150 for china. this is years of accumulated compliance work that a new entrant cannot replicate quickly.

Why inox india sometimes loses. On the cryo scientific side, european institutions have historical preferences for established european suppliers. The competition for the fair project in germany involves competitors who are geographically proximate and have stronger local relationships. On large-scale lng infrastructure, chart industries and linde engineering have capabilities that inox india has not yet demonstrated at scale.

Chinese competition is the emerging threat on standard industrial gas tanks. chinese manufacturers can also manufacture at low cost, hold relevant certifications, and are aggressively marketing globally. inox india’s moat here is quality consistency, certification breadth, and relationships - not a fundamental technology advantage on standard products. management flagged in the q4 fy25 concall that securing an australia order for oxygen, nitrogen, and co2 imo containers “positions us in direct competition with chinese” manufacturers - suggesting the company views this as a meaningful competitive battleground.

Domestic competition is limited for the specialized products. there is no credible indian competitor in cryo scientific, no competing indian manufacturer of iter transfer lines, and no other indian manufacturer with iatf 16949 certification for cryogenic fuel tanks. For standard industrial gas tanks in india, inox india has an effective domestic monopoly among larger orders.

Industry

Demand drivers. the fundamental demand for cryogenic equipment comes from several converging trends: (1) industrial gas consumption growth, driven by steel, chemicals, healthcare, and food processing expansion; (2) lng infrastructure buildout globally as gas replaces coal in power generation; (3) the energy transition and the role of lng as a “bridge fuel” for heavy transport and island economies; (4) green hydrogen, which requires cryogenic storage and transport at -253°c (liquid hydrogen); and (5) scientific and government research spending on fusion energy, space programs, and particle physics.

Market size. The global cryogenic equipment market (broadly defined) was valued at approximately usd 26-27 billion in 2025 across various research estimates, with forecasts ranging from 7% to 10% cagr through 2032-2035, implying a market roughly doubling in size over a decade. The more focused cryogenic tanks/vessels sub-market was around usd 7-8.5 billion in 2025. Asia-pacific dominates with approximately 35-47% of global demand, driven by china, india, japan, and south korea.

India-specific drivers. India’s manufacturing sector is the largest consumer of industrial gases domestically, accounting for approximately 45% of the market in 2024 per the mncl research note - driven primarily by steel, which uses oxygen and nitrogen extensively. India’s steel capacity expansion (multiple large greenfield projects) will require corresponding industrial gas infrastructure. The government’s semiconductor push - a usd 8.87 billion program with 6 fabs approved and 5 more under construction by mid-2025 - creates demand for ultra-high purity gas delivery systems. and india’s lng adoption as a vehicle fuel, while slower than initially hoped, is expanding as the regulatory framework (smpv rules) has been updated to approve lng vehicles.

Regulation. Cryogenic equipment is heavily regulated because the gases involved (oxygen, lng, hydrogen) are either oxidizers, flammables, or asphyxiants at scale. every major market has its own pressure vessel standards (asme in the us, ped in europe, etc.) and inspection/certification requirements. This regulation creates a barrier to entry that favors incumbents with established certifications. It also makes switching suppliers more costly and slower for customers, since a new supplier must go through the same certification process. India’s own peso (petroleum and explosives safety organisation) regulations govern the installation and operation of cryogenic systems domestically.

Cyclicality. The industrial gas segment is relatively stable - gas companies make recurring capital investments in storage and distribution as they add capacity or upgrade old tanks. The lng infrastructure segment has project-driven lumpiness. The cryo scientific segment is the most lumpy, driven by funding cycles of scientific institutions that can be unpredictable. the vehicle fuel tank segment (if it scales) would be more regular, tracking truck production volumes and adoption of lng powertrains.

The chinese factor. Chinese manufacturers (primarily zhangjiagang cimc sanctum and associated entities) have been expanding their presence in global cryogenic equipment markets, particularly for standard-specification industrial gas tanks. They carry the relevant certifications and can match inox india on price in some segments. This competitive pressure has been intensifying and is the single most important structural threat to inox india’s standard-product order flow over the next 5 years.

Growth Triggers

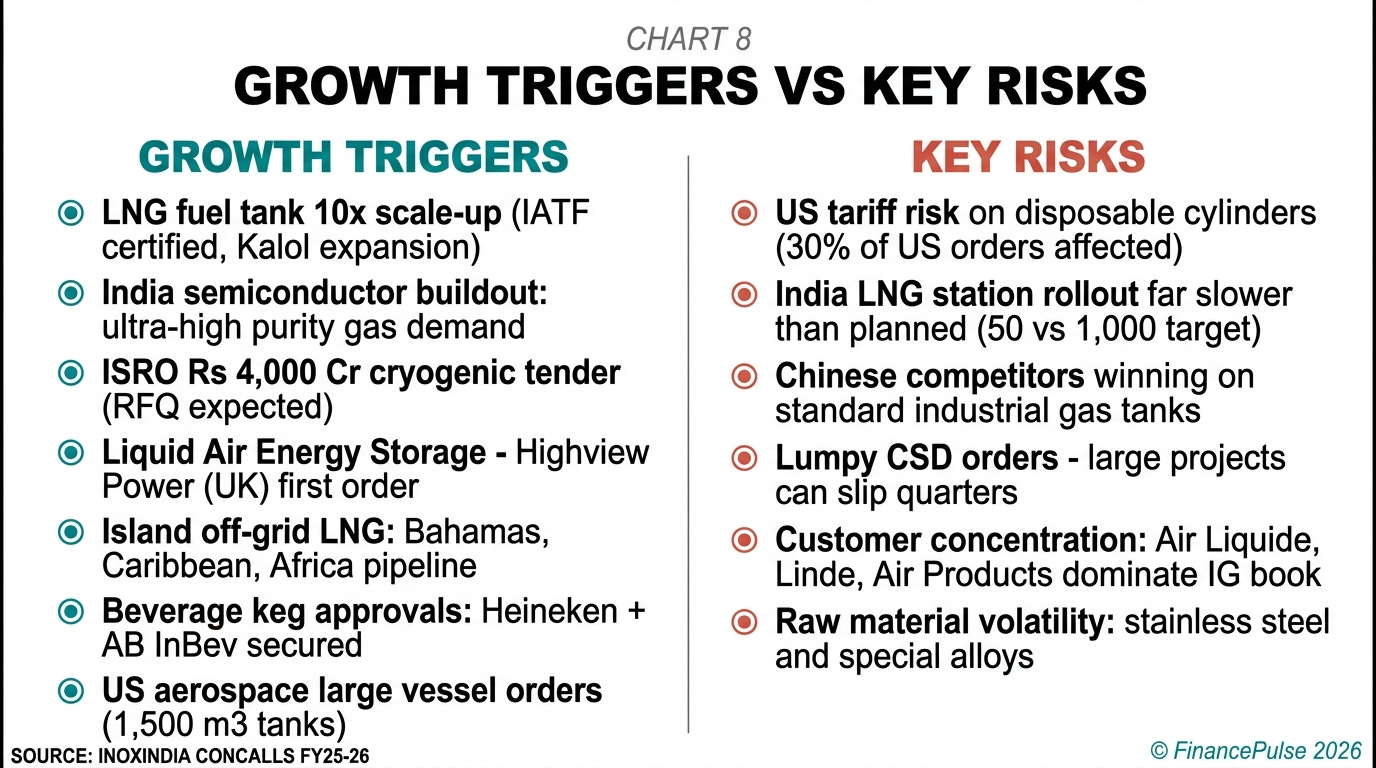

LNG vehicle fuel tank scale-up: Management stated on the q1 fy26 concall that the company was “expanding capacity and building capabilities to scale our lng drill tank production up by 10x over the next few years, supported by favourable regulatory changes and increasing domestic and export demand.” The iatf 16949 certification (february 2025) removed the key barrier to oem supply and the kalol plant has dedicated production lines. management described lng as a “winner fuel for 8-10 years.”

Semiconductor and high-purity gas applications: Management called india’s semiconductor buildout - rs 1.6 lakh crore in planned investment - as “very bullish” for inox india’s prospects. The company delivered 9 tanks to a us semiconductor customer in q4 fy25 and launched india’s first ultra-high purity ammonia iso containers in q1 fy26. Management stated: “almost 75% projects are coming” online.

ISRO and space infrastructure: Management noted active engagement with isro on a large cryogenic systems tender, expected rfq by december 2025. separately, the company is bidding for the fair (facility for antiproton and ion research) project in germany. cryo scientific orders are large, lumpy, and high-margin.

Island and off-grid lng infrastructure: The bahamas project (10 x 1,500 m3 tanks, awarded november 2024) was followed in q2 fy26 by two additional island power station projects in the caribbean. Management described these as “part of a broader island energy infrastructure development plan.” islands without pipeline access represent a recurring market for mini-lng terminals globally - the company’s execution in the bahamas and antigua creates a reference portfolio that is hard to replicate.

US aerospace and large vessel orders: management confirmed receipt of orders from a “leading us-based aerospace company” for 2 x 1,500 m3 cryogenic storage tanks in q2 fy26 (november 2025 concall) and again in q3 fy26 (february 2026 concall). Aerospace and space launch customers are new and high-value. management described it as demonstrating “customer confidence in inox india’s engineering capabilities.”

liquid air energy storage (laes) - new segment: inox india delivered 5 x 690 kl cryogenic storage tanks to highview power (uk) for the world’s first commercial-scale liquid air energy storage facility in carrington, manchester. management called this the company’s “first order for a liquid air energy storage project.” laes stores electricity by liquefying air during cheap/excess generation, then re-expanding it through a turbine when power is needed - a grid-scale battery concept. if laes scales globally, this creates a new demand vector for large cryogenic tanks.

beverage keg approvals secured: management confirmed on the q3 fy26 concall that both heineken and ab inbev approvals had been secured, giving the company approximately 40% exposure in the stainless steel keg market. the peak brewing season (january to july) should convert these approvals into meaningful revenue.

co2 battery storage and new applications (q1 fy26): the company launched co2 battery storage as a product category and secured a pilot order from italy. while still early stage, management described “global potential” for this application.

Key Risks

US tariff exposure on disposable cylinders. the disposable refrigerant cylinder segment relies heavily on us customers. Tariffs on indian-manufactured goods sold into the us market were flagged explicitly in q4 fy25 - management acknowledged that tariff uncertainty caused customers to pause orders, saying “people were just waiting because they are confused what to do... we were almost having ready tanks available at our shop almost 2 million to 2.5 million and people were just waiting.” The company ultimately negotiated duty pass-through with some customers, but this remains live. A significant tariff escalation (which us policy in 2025 made more plausible) could materially reduce the disposable cylinder order book from the us.

LNG adoption pace risk - india stations. The thesis on lng vehicle adoption includes a vision of 1,000+ lng dispensing stations along indian highways. Actual build-out has been dramatically slower. Management explicitly admitted on the q2 fy26 concall that “lng station somehow is not picking up that fast to our expectation.” If the station buildout remains slow, the vehicle fuel tank business grows much more slowly than the 10x capacity expansion plan implies - that capacity would sit underutilized.

Lumpy order book and revenue concentration. The cryo scientific division is inherently project-driven. Management has consistently noted that order inflows in q3 fy26 were rs 392 crore against a targeted rs 450+ crore, partly because large csd and lng orders “did not materialize in q3.” If a few large orders slip quarters, reported revenue and margins can be significantly affected. This is not unique to inox india, but it means that quarterly numbers will be volatile around the trend.

Chinese competition on standard products. Chinese manufacturers are qualified on asme, ce, and other standards, and can compete on both price and delivery for standard industrial gas tanks. Inox india’s advantage on standard products is gradually narrowing. the company’s response has been to move up the value chain (aerospace tanks, semiconductor applications, laes, iter) where chinese competition is less developed, but the standard product segment is a meaningful portion of current revenue.

Customer concentration in key segments. While the industrial gas segment serves air liquide, linde, and air products globally, these three companies together likely represent a significant share of the industrial gas division order book. Any strategic shift by one of them - building internal tank manufacturing, qualifying a chinese supplier, or slowing their own capex - would have a disproportionate effect on inox india.

Raw material costs. stainless steel and special alloys are the primary inputs. price volatility in these materials affects margins, especially on fixed-price contracts. The q3 fy26 concall noted “gross margins were slightly lower this quarter, attributed to fluctuations in commodity prices and project-specific factors.”

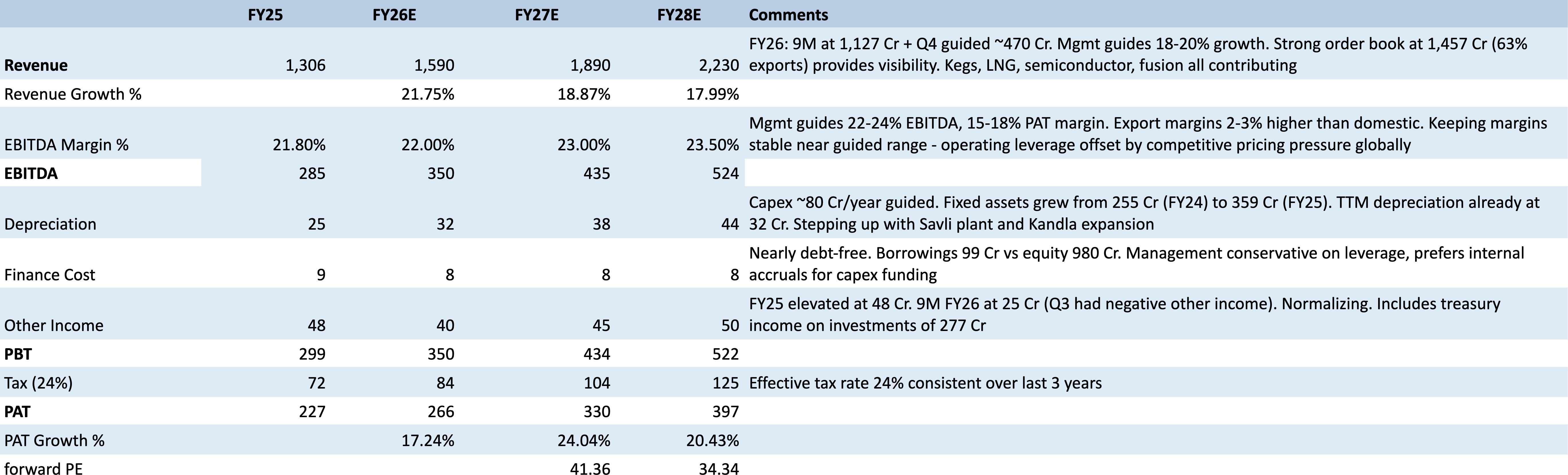

Valuation & Scenario Analysis

Bull case

The convergence of three demand vectors turns inox india into a much larger company by fy28-29. First: india’s semiconductor manufacturing buildout - six fabs approved by mid-2025 with five more under construction - creates a wave of demand for ultra-high purity gas systems and specialized cryogenic storage. Inox india has positioned itself with the right products (ammonia iso containers, helium systems) ahead of this demand. Second: the 10x scale-up of lng fuel tank production at kalol, enabled by iatf certification and supported by oem adoption from tata motors and ashok leyland, turns the vehicle fuel tank business from a niche into a meaningful segment. If india deploys even 100,000 lng trucks over the next five years, that is a sustained manufacturing program. Third: the isro and scientific project pipeline materializes - an isro cryogenic systems order, the fair project in germany, and follow-on iter work all arrive within the same 18-24 month window. CYRO scientific margins are high, the projects are milestone-based, and each win creates a reference for the next.

Base case

Inox india grows steadily at the 18-20% revenue growth pace management has guided. The industrial gas segment continues to compound off a growing global gas infrastructure base. The LNG segment contributes through vehicle fuel tanks (kalol expansion bears partial fruit) and episodic turnkey project wins (one or two island/mini-terminal projects per year). The cryo scientific segment delivers lumpy but accretive revenue from iter refurbishment work, some isro contracts, and potentially fair project participation. The keg approvals from heineken and ab inbev add incremental volume. Exports remain 55-65% of revenue. The company does not face a severe tariff shock or a major customer loss. The order backlog stays in the rs 1,400-1,600 crore range, providing 9-12 months of revenue visibility at any given time. This is the trajectory the last three quarters of fy26 suggest - steady, above-market, but not transformative.

Bear case

Two things go wrong at the same time: us tariffs on disposable cylinders escalate materially, causing the us cylinder order book to dry up, and the lng vehicle fuel tank business continues to grow slowly because the station infrastructure rollout remains stuck at 50-100 stations rather than scaling to the government’s 1,000-station vision. The cryo scientific segment delivers no new large orders for 12-18 months because isro’s rfq process drags on and the fair project award goes to a european competitor. In this scenario, revenue growth slows to high-single-digits to low-teens. The savli plant runs at reduced utilization, creating operating leverage headwinds. The standard industrial gas tank business faces increasing pressure from chinese competitors who are winning at the margin on price-sensitive mid-complexity orders. The keg business is delayed further because brewery approvals, while secured, do not translate to volume until fy28. The company remains profitable and the balance sheet stays healthy (net debt was minimal through fy25 and fy26), but the growth story that attracted investors at ipo is less compelling than it appeared.

Thanks for reading! Do check out Investorstack.